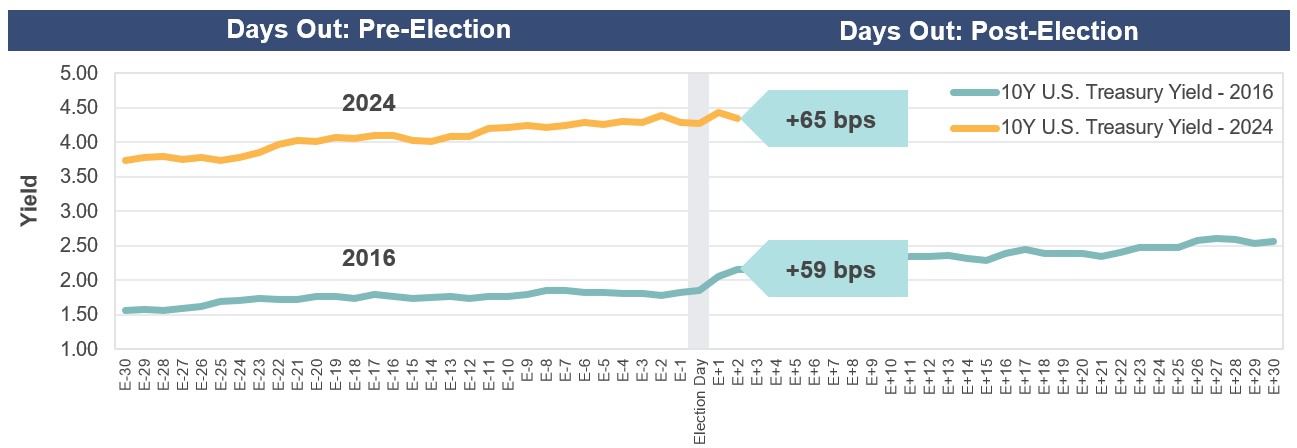

Despite the beginning of a Federal Reserve (Fed) rate easing cycle, longer-term rates have spiked higher following the 50 basis point rate cut on September 18. U.S. Treasury bonds across the curve have seen their yield rise dramatically with notably the 5-year note up over 80 bps. The entire U.S. Treasury yield curve now yields over 4.00%. Yields are trading in a narrow range from 4.25% on the 3-year note to 4.70% on the 20-year note. This rate increase has continued into November even though the Fed cut rates again by 25 bps on the earlier this month.

Several factors that have driven this rate increase. Importantly, economic data continues to remain strong in both jobs and growth. Annualized U.S. Real Gross Domestic Product (GDP) for the third quarter was a solid 2.80%. Unemployment remains just above its all-time low of 4.10%. While inflation materially eased from the post-pandemic peak, it remains well above the Fed’s goal of 2.00%. Since June, progress on the inflation front has moderated as growth has remained resilient with the U.S. Personal Consumption Expenditure Core Index posting a solid 2.70% in 3Q24. The resiliency of this number is important as the Fed weighs the speed and depth of any cuts going forward.

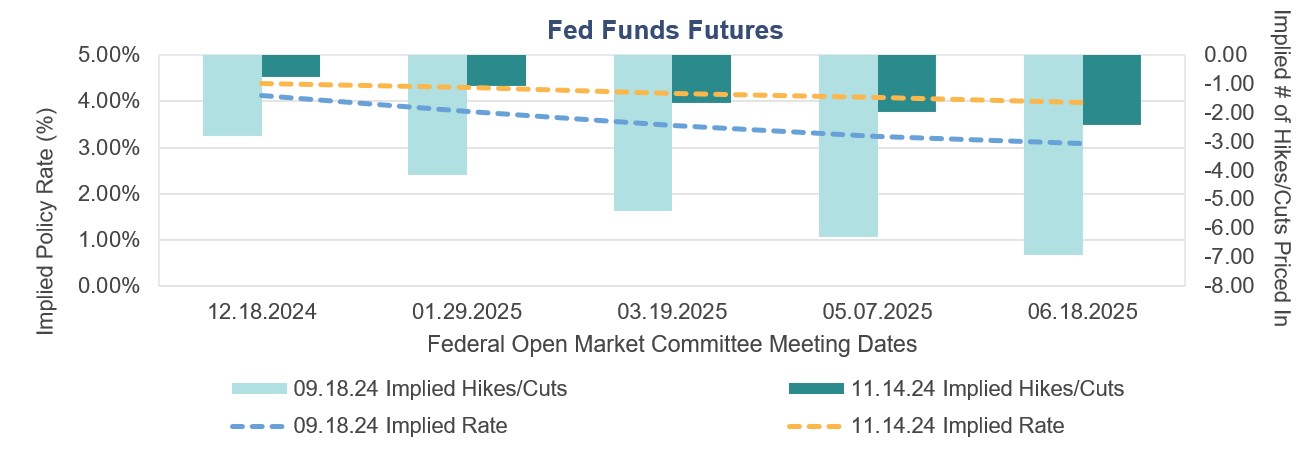

U.S. economic strength, and particularly the stickiness of inflation and wage inflation, has caused the market to reassess the need for future cuts by the Fed. After the Federal Reserve Open Market Committee (FOMC) rate cut on September 18th, the market expectation was for the fed funds rate to fall to 3.00% in the third quarter of 2025. These expectations have changed markedly in two months. Now the market is pricing in only an additional 75 bps of cuts and the rate to fall to 4.00%, a 100-bps adjustment upward. This has been a catalyst for the rest of the yield curve to adjust up as well.

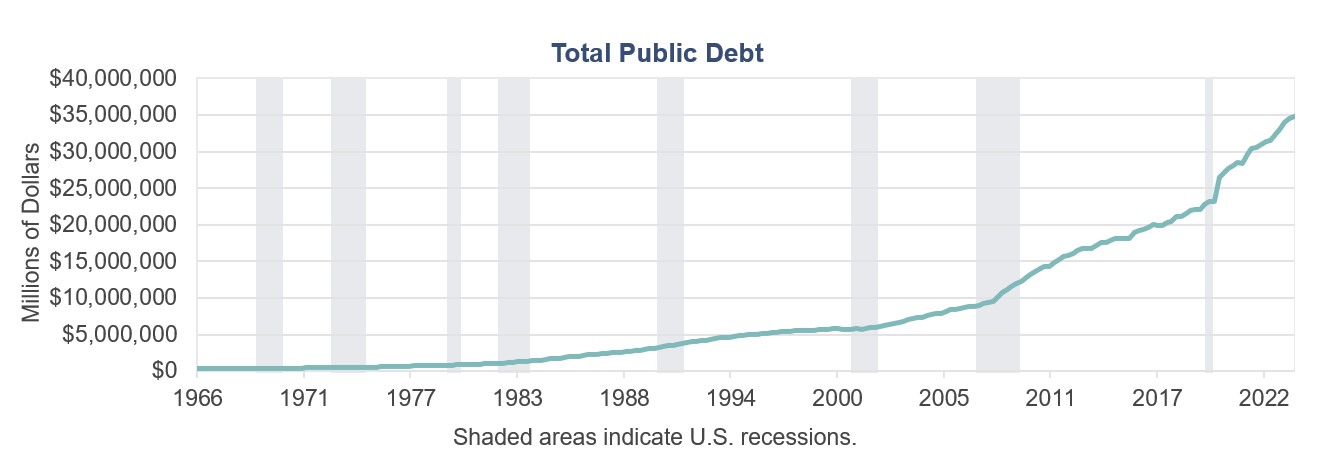

Another factor the bond market is now grappling with is the burgeoning U.S. deficit. While the deficit has been ballooning higher for several years now, post-COVID-19 we have seen this debt burden ramp up. Given the persistent inflation we referenced above, and the fact that the Fed is now in a rate cutting cycle, a renewed focus by the market has resulted in a push back against these levels and helped to send rates higher. Such actions are commonly referred to as “bond vigilantes”. Adding to this deficit is the fact that fiscal policy has been loose under past administrations, and there is now little expectation for restraint in the near term. Finally, the likelihood of the tax cuts that were enacted in 2017, known as the Tax Cuts and Jobs Act becoming extended when they are set to expire next year has increased with President-elect Trump’s victory, as have the odds for trading tariffs with foreign counterparties.

About the Author

Andrew Richman, CTFA, Managing Director, joined SunTrust in 2001 and SCM in 2020 as part of an integration following the merger of equals between SunTrust Banks and BB&T Corporation. Andy has investment experience since 1988 and is a Fixed Income Portfolio Manager and Senior Fixed Income Client Strategist. Prior to his 20 years in SunTrust’s portfolio management division, Andy ran a trust and investment department in Florida as the trust department senior manager and worked as an equity portfolio manager with Sanford Bernstein. He received his B.A. from the State University of New York at Albany and his M.B.A. with a concentration in International Business from the University of Miami. He is also a graduate of the ABA National Trust School at Northwestern University and holds the Certified Trust & Financial Advisor designation.

Related Insights

07.02.2025 • Charles Wittmann, CFA®

06.20.2025 • Andrew Richman, CTFA

06.10.2025 • Charles Wittmann, CFA®

05.07.2025 • Charles Wittmann, CFA®

Explore