Fixed income security prices and interest rates generally move in opposite directions. When market yields fall, the discounted present value of a fixed stream of cash flows is worth more, and likewise is worth less when yields rise. Each security’s sensitivity to changes in interest rates is measured by the bond’s duration. Duration, defined as weighted average time until cash flows are received (in years), is more commonly thought of as an estimate of the sensitivity of a bond’s price to changes in interest rates. For example, if we had a bond with a duration of six years and yields fell by 50 basis points (bps), we would estimate that the immediate impact of that rate decline would cause the price of that bond to increase by approximately 3% (0.50% rate move x 6-year duration = 3%).

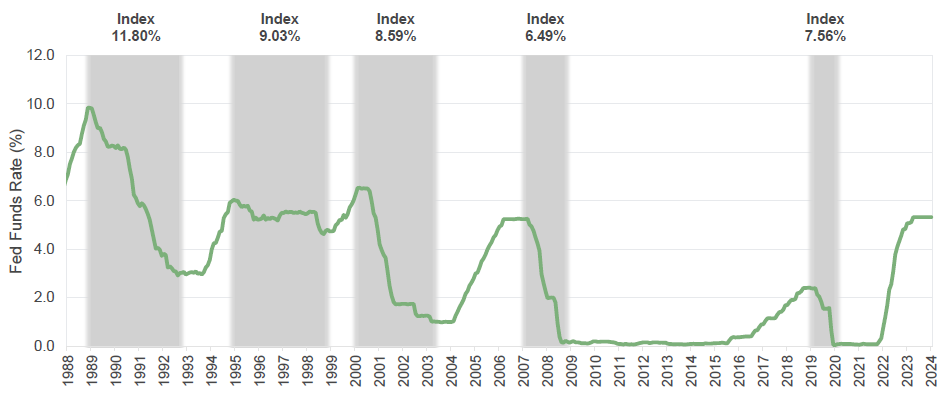

As one would expect, in most historical periods where interest rates were declining, fixed income total return has been good, with investors capturing coupon income as well as benefiting from the increase in prices as rates fall. Looking at the history of the Bloomberg Aggregate Bond Index since 1988, in the previous five Federal Reserve (Fed) rate-cutting cycles, the index posted annualized returns averaging north of 8%, as illustrated below.

That said, interest rate duration isn’t the whole story. The reason for the decline of interest rates also matters, as the macroeconomic environment will also impact risk premiums, or spreads, of fixed income securities relative to Treasuries with similar durations.

To get a better estimate for fixed income performance (and to make better decisions as to what types of fixed income we’d like to own) we also need to consider a bond’s exposure to changes in these risk premiums, which is where spread duration comes in. Spread duration measures the sensitivity of a bond’s price with respect to changes in the required spread over Treasuries of an equal maturity. Its impact on bond pricing is very similar to that of duration and regular changes in rates in that as required spreads rise, bond prices fall, and vice versa. Spread changes are often a large driver of how the various fixed income subsectors perform relative to Treasuries and, as such, are key to any fixed income outlook, in our view.

1The index total return periods include one additional month before and after each cycle to reflect market expectations and reactions. Returns are annualized for periods greater than one year. Fed funds rate data is as of 05.31.2024. Performance is compared to an index: however, the volatility of an index varies greatly and investments cannot be made directly in an index. Market conditions vary from year to year and can result in a decline in market value due to material market or

economic conditions. Sources: Bloomberg L.P.; Federal Reserve Economic Data. Yields are subject to market conditions and are therefore expected to fluctuate. Charts are for illustrative purposes only. The views expressed represent the opinions of Sterling Capital Management. Any type of investing involves risk and there are no guarantees that these methods will be successful. The performance presented represents past performance and is no guarantee of future results.

About the Author

Jeffrey Ormsby, CFA®, Executive Director, joined SCM in 2010 and has investment experience since 2006. Jeff is a Senior Fixed Income Portfolio Manager. Prior to joining SCM, he worked for Smith Breeden Associates as a CMBS trader and portfolio management analyst within the investments group. Jeff received his B.S. in Economics from North Carolina State University, where he was a summa cum laude graduate and was recognized as Valedictorian, and his M.B.A. from the University of North Carolina at Chapel Hill’s Kenan-Flagler Business School, where he was the Norman Block Valedictorian Award recipient. He holds the Chartered Financial Analyst® designation.

Related Insights

03.28.2025 • James Kerin, CFA®

01.27.2025 • Andrew Richman, CTFA

Meet Andrew Richman, Sterling Capital Managing Director and Senior Fixed Income Client Strategist

12.12.2024 • Orton Chen, CFA®

Meet Orton Chen, Chief Investment Officer for Sterling Capital's Private Client Group

11.22.2024 • Shane Burke

Meet Shane Burke, Sterling Capital Advisory Solutions Portfolio Manager

Explore