The market has spent much of the last two years fixated on the negative effects of rising rates on Real Estate Investment Trust (REIT) share prices. What has received less attention is the slowdown in new developments of commercial and multifamily real estate due to higher interest rates and the potential for higher rents in coming years should consistent demand growth be unmet by new supply. We believe publicly-traded REITs, which derive much of their earnings growth from existing real estate rather than new development, are overlooked future beneficiaries of this construction slowdown.

Prior to March of 2022, the Fed Funds Rate had stood in a range of 0-50 basis points (bps) since the Great Financial Crisis (GFC) of 2007-2008 and longer-term interest rates were similarly near all-time lows. As a result, borrowing costs were historically cheap and new construction of all types of commercial real estate and apartments boomed. Today’s higher rates are making development uneconomic and putting the brakes on new construction. The coming slowdown in fresh supply of real estate should be beneficial to cash flows for owners of existing real estate, in our view.

Herein we examine data showing the decline in overall new construction of commercial properties and focus on data for several property types that collectively make up over half of the major REIT benchmarks.

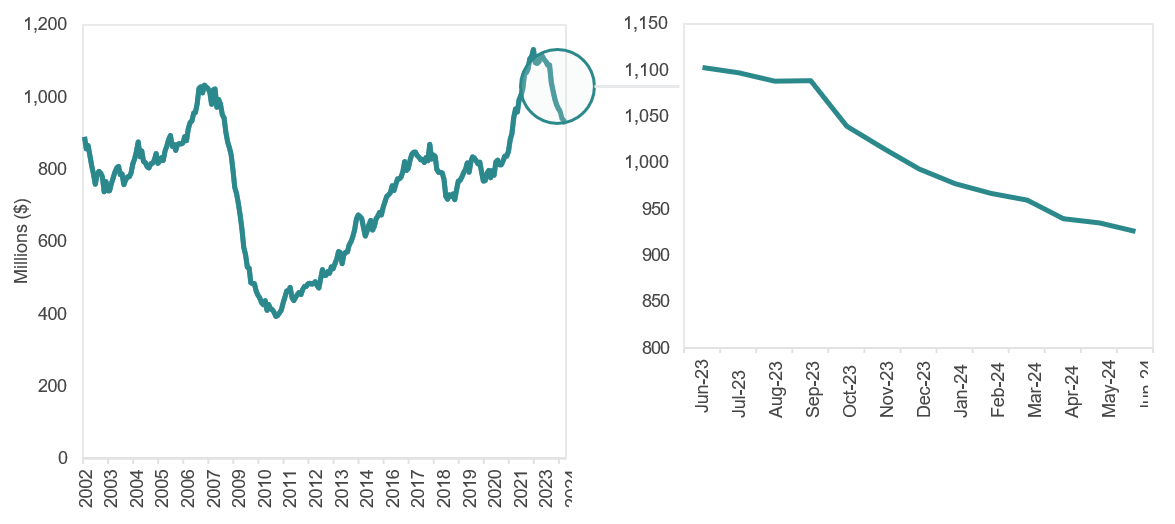

U.S. Commercial Construction Trending Lower

The total dollar value of commercial construction underway in the United States declined substantially following the GFC before gradually recovering in the following 12 years. In the aftermath of the COVID-19 pandemic, amidst record low interest rates, construction shot up further, reaching an inflation-adjusted level on par to the prior 2007 peak. However, as higher Fed Funds rates flowed through into construction loan interest rates, spending has inflected lower with new construction starts trailing completions.

Leading Indicators Suggest a Continued Commercial Construction Slowdown

The Architectural Billings Index, a leading indicator for nonresidential construction activity with a historic lead time of 9-12 months, has been in contraction territory since August 2023. The Dodge Momentum Index, published monthly by McGraw-Hill Construction Analytics, declined from the middle of 2023 through May 2024, and is typically a 12-month leading indicator of construction spending for nonresidential buildings. While the Dodge Index has inflected upward the last two months, the improvement was primarily credited, by Dodge, to “data center planning” as well as hospital construction. In our view, this suggests apartment and non-data center commercial real estate development will remain sluggish.

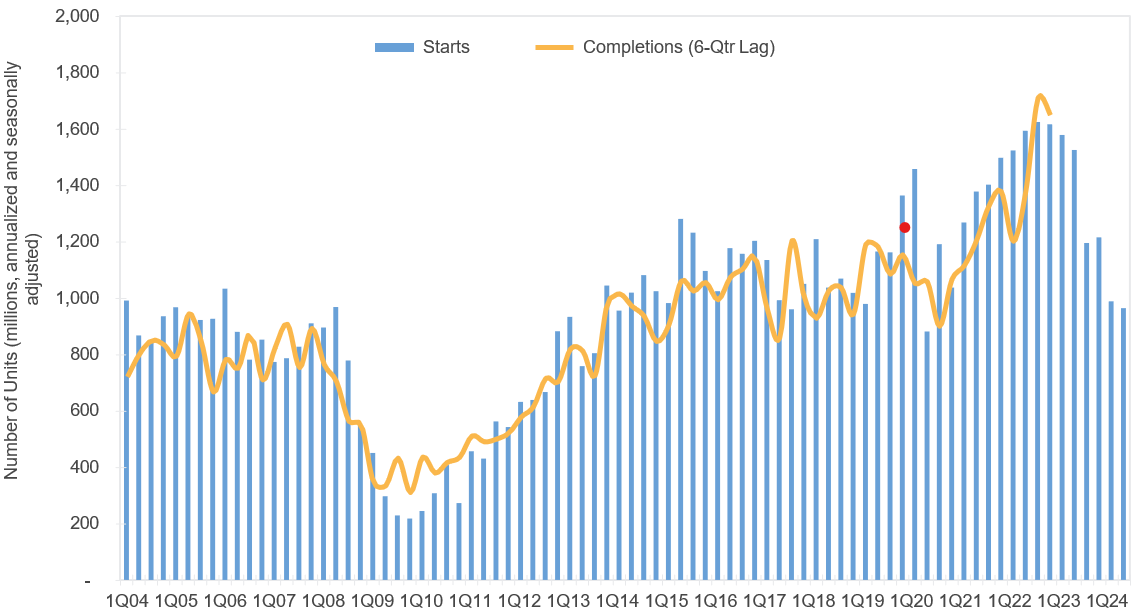

Residential REITs (15% of the Bloomberg U.S. REIT Index)

The post-COVID-19 rise in apartment rents has been a frequent theme in news stories focused on inflation drivers, though many highlight the expectation for 2024’s record new supply to reverse the trend by putting downward pressure on rent in the near future. However, looking beyond the current year, the data suggests new deliveries may fall. New construction starts have recently slowed to near long-term averages and commentary from REIT management teams during quarterly conference calls suggests starts may fall further. As shown below, the record amount of 2024 deliveries is a result of record new construction starts approximately 18 months ago. The subsequent slowdown in starts suggests fewer deliveries in 2025 and 2026, which should return pricing power to landlords.

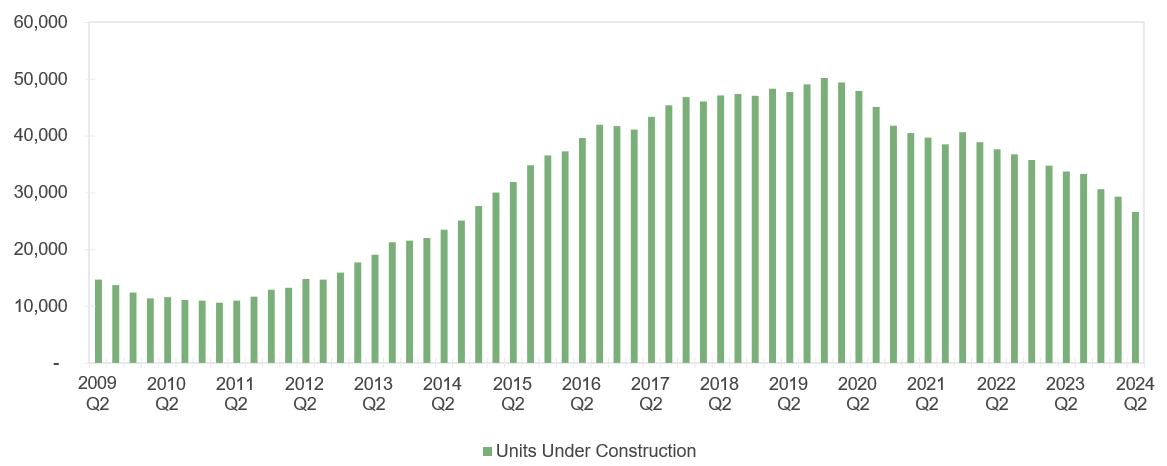

Retail REITs (14% of the Bloomberg U.S. REIT Index)

Construction of new retail space boomed during the mid-2000s as new shopping centers “followed the rooftops” of the single-family building craze that eventually led to the GFC later in the decade. As shown below, new retail construction declined markedly following 2008 and has remained at a low level.

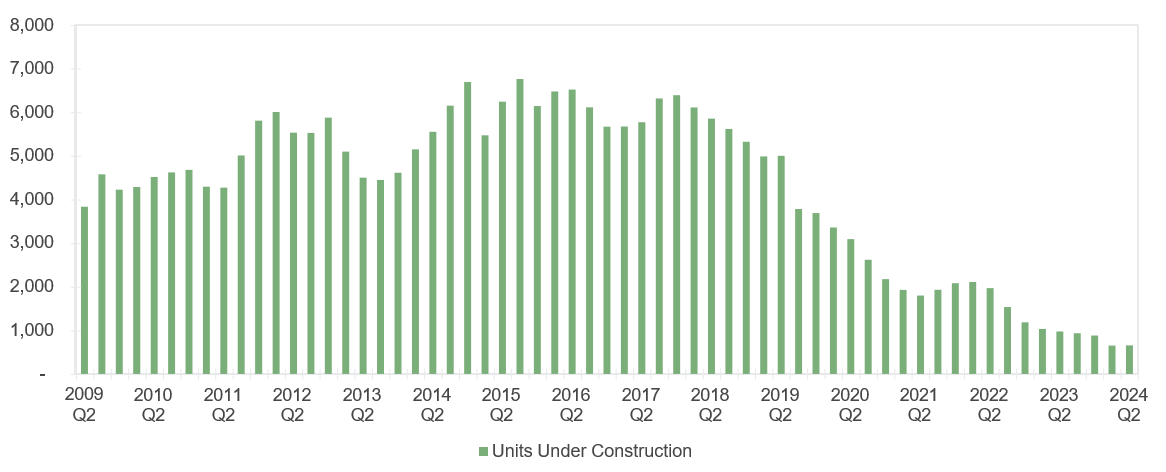

Healthcare REITs (10% of the Bloomberg U.S. REIT Index)

The healthcare subsector is dominated by REITs focused on two types of real estate – senior living properties and skilled nursing facilities. Construction of both property types was already declining ahead of the pandemic, due to oversupply of senior living and declining demand for skilled nursing. The immediate effects of post-COVID-19 regulatory scrutiny on both businesses kept new supply in check during the low-rate environment of 2020-2022, and higher interest rates are continuing to limit construction.

About the Author

Andrew DiZio, CFA®, Executive Director, joined the Stratton Funds team of Stratton Management Company in 2012 and SCM as part of a business acquisition in 2015. He has investment experience since 2003. Andy is Portfolio Manager of the Mid Cap Relative Value and Real Estate strategies, Co-Portfolio Manager of the Mid Cap Value Fundamental strategy, and Associate Portfolio Manager of the Small Cap Value strategy. Prior to joining SCM, he was Vice President at Janney Montgomery Scott where he served as a real estate investment trust sector analyst. Andy received his B.S. in Finance with a minor in Economics from Pennsylvania State University. He holds the Chartered Financial Analyst® designation and is a member of the CFA® Society of Philadelphia and the CFA® Institute.

Related Insights

07.02.2025 • Charles Wittmann, CFA®

06.20.2025 • Andrew Richman, CTFA

06.10.2025 • Charles Wittmann, CFA®

05.07.2025 • Charles Wittmann, CFA®

Explore