Executive Summary

Collateralized loan obligations (CLOs) are actively-managed securitized pools of leveraged loans, providing floating-rate exposure to corporate credit risk. CLOs are cash-flow oriented rather than mark-to-market (MTM) oriented by design, allowing the structure to withstand and even benefit from price volatility in the leveraged loan market. With substantial protections for investment-grade CLO investors, as demonstrated by zero AAA-rated tranche defaults and extremely rare AA- and A-rated defaults in the more than 35-year history of the market, we believe that CLOs can provide diversification benefits and enhance risk-adjusted portfolio returns.1

Background

What is a securitization?

When debt is originated by a bank or finance company, whether in the form of a loan to a business or mortgage to a consumer, it can be retained on a balance sheet or sold into a securitization like a CLO. When sold and placed into a securitization, the debt becomes an asset in the securitization’s collateral pool, with its purchase ultimately funded by the investors who purchase the securitization’s interest-bearing securities, also referred to as CLO liabilities or debt tranches. The collateral pool generates the cash flows required to service these securities over time. In essence, the bank has effectively traded places with the new group of securitization investors who assume the credit risk of the loans.

What are leveraged loans?

Leveraged loans, sometimes referred to as leveraged bank loans, are loans made by banks to below-investment-grade companies considered to have a higher risk of defaulting, often as a part of merger, acquisition, or leveraged buyout (LBO) activity. Leveraged loans are typically first lien, meaning that they have first claim on the assets of the underlying business in bankruptcy and therefore top priority in recovering principal relative to other debtholders. The leveraged loan market is ubiquitous, with American Airlines, Hilton Hotels, Dell, Burger King, and many other household names issuing in this market historically. Today, the market funds well over $1T in loans to U.S. businesses that collectively employ millions of Americans2.

Businesses with earnings before interest, taxes, depreciation, and amortization (EBITDA) above $100MM3 are generally considered large enough to receive a broadly-syndicated loan (BSL). BSLs are originated by a group of banks working together to jointly fund and syndicate, or allocate, the exposure. Below the $100MM threshold, the loan is considered to exist within the middle market or private credit (MM/PC) space, where loans are originated by a smaller group of lenders. Over the last ten years, CLO and leveraged loan markets have grown increasingly intertwined, with CLO loan holdings going from approximately 45% to over 70% of the market’s total leveraged loans outstanding over the period4.

What does it mean for leveraged loans to be floating rate?

The interest rate paid by floating leveraged loans are based on the Secured Overnight Financing Rate, or SOFR. SOFR is published daily by the Federal Reserve Bank of New York and reflects the cost of secured overnight borrowing collateralized by Treasury securities. Both leveraged loans and CLOs calculate their coupons paid to investors using two components that are summed together: first, a Term SOFR rate, which is reset periodically, and second, a spread that is determined at issuance. Term SOFR is a forward-looking rate based on the derivatives markets published by the CME Group for various periods, such as one month, three months, etc. Importantly, both the assets and liabilities of a CLO are required to have a reference rate of Term SOFR by the governing legal documents with few exceptions, minimizing the risk of interest rate volatility causing a destabilizing structural issue for the CLO.

What is the role of a CLO manager?

CLOs are actively managed by specialized asset management companies. Each CLO holds hundreds of leveraged loans that are diversified across a swath of industries, with each loan scrutinized for its creditworthiness continuously throughout its life. Once purchased by a CLO manager, the loans are directly monitored both by public rating agencies and dedicated teams of specialized CLO credit analysts. The loans are also indirectly monitored by CLO investors who analyze aggregate measures of collateral pool performance reported on a monthly basis.

Importantly, when economic growth slows and prices in the leveraged loan market decline, CLO managers are a natural buyer of loans, reinvesting loan repayments into new loans at more attractive levels during the reinvestment period (more on this below). Furthermore, managers may trade in and out of leveraged loans in an effort to add relative value, provided that they do not run afoul of various collateral pool guardrails that require certain levels of credit quality, spread, and average life to be maintained. CLO investors also track changes in CLO collateral composition to ensure that CLO managers are following their stated style, whether that be more aggressive or conservative in nature.

Structure

What is the structure of a CLO and what investor protections does it provide?

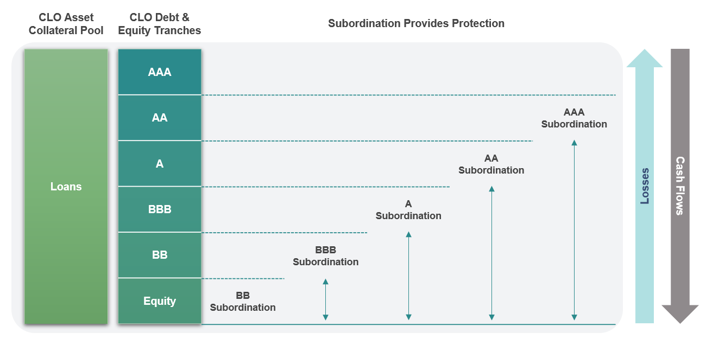

CLOs are structured such that lower-rated debt tranches provide par subordination, or credit support, to higher-rated debt tranches. Cash flows from the leveraged loans are sequentially paid to senior liabilities starting with the AAA tranche and ending with the BB tranche, with excess cash flows retained by CLO equity bondholders. On the other hand, principal losses are absorbed first by CLO equity, then by the BB tranche, and so on until the AAA tranche. This structure results in vastly different risk/return profiles for each debt tranche. While the AAA tranche takes relatively little credit risk, it also earns the lowest floating-rate coupon, receives the first cash flows, and has the shortest life. In contrast, the BB tranche earns a materially higher coupon, is much more exposed to losses, and remains outstanding the longest.

Today, CLOs are typically issued with par subordination of roughly 35%, meaning that the loan collateral would have to take 35% in principal losses before the AAA-rated tranche would begin to take losses. For comparison, in the Great Financial Crisis (GFC) of 2007-2008, the leveraged loan market experienced a peak default rate of 11%5. But defaults are not principal losses: the vast majority of CLO collateral are first lien, where loan recoveries are significant following default, averaging 73% over the long term6. In addition, AAA par subordination has increased by approximately 10% since the GFC, augmenting credit support for the tranche7.

CLO performance metrics also provide critical investor protections, generally referred to as “self-healing” mechanisms. If key thresholds are breached, the trustee of the CLO must either divert cash away from the equity and junior tranches to either buy more collateral or pay down the senior debt tranche, whichever is dictated by the CLO indenture. As a result, paradoxically, worse loan performance will often result in faster AAA repayment. There is no mechanism to force the sale of loans from the collateral pool, barring an event of default as defined in the indenture.

What is the life cycle of a CLO?

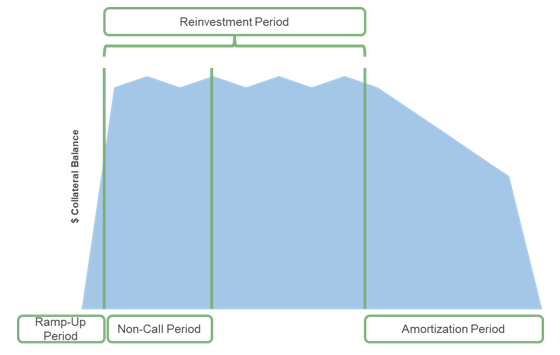

CLOs are typically issued with an initial two-year non-call period and five-year reinvestment period, though there are many variants. The reinvestment period requires the CLO manager to reinvest loan prepayments and maturities into new loans. Once the reinvestment period ends, the CLO manager has a more limited ability to recycle loan principal into new collateral and must follow well-defined portfolio criteria to begin using principal paydowns to amortize the CLO liabilities, beginning with the AAA tranche.

The non-call period guarantees that the CLO will remain outstanding until the periods ends. Once the non-call period ends and the CLO becomes callable, however, it may be refinanced or reset at the discretion of the majority CLO equity holder. In a refinance, the CLO lowers its cost of capital by re-issuing its debt liabilities at the prevailing market rate, with the flexibility to refinance as many or as few tranches as desired. In a reset, however, all of the debt liabilities are paid off and more substantive changes are made to the indenture, which often includes extending the life of the CLO via resetting the reinvestment period to a further end date. In all instances, CLO investors can decide to roll their principal into the new CLO or have the principal returned at par. The CLO equity can also liquidate the entire deal, selling all the collateral and paying off the liabilities held by investors.

What are the economics of a CLO?

In the BSL market, the CLO manager’s business model is effectively an arbitrage of the excess spread to be found in the leveraged loan market above the borrowing cost of the CLO liability stack. Each dollar borrowed from CLO liability investors and used to buy a higher-yielding loan increases the leverage of the CLO. Critically, CLO equity is about 2% higher today relative to pre-GFC vintages, meaning CLOs today have less borrowing in them, or leverage, another example of how the structure has improved over time8.

In contrast, the smaller loan size and naturally limited ownership groups in MM/PC lead to a much less liquid market environment where loans are often held to maturity. As a result, while the economics of the CLO operate under the same principles, MM/PC CLOs are primarily a form of new loan financing for the originating companies rather than a market arbitrage strategy, serving to free up capital from old loans that the finance companies can redeploy into new ones.

AAA CLO Performance Risks & Outlook

What are historical default rates for CLOs?

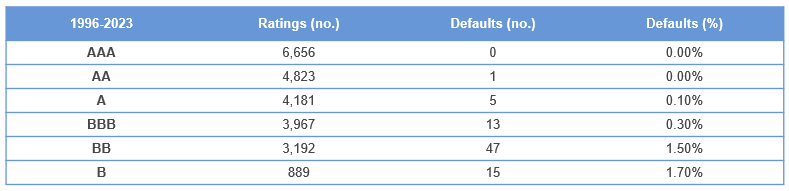

According to S&P ratings, no AAA-rated CLO has ever defaulted in the recorded history of the CLO market, dating back to 1996. Of note, the single AA-rated CLO default shown below paid in full, as well as interest on interest, following the resolution of a legal action in 2011 that temporarily resulted in the setting aside of the note’s interest payments.

Defaults for A and BBB tranches are rare as well. In total, the cumulative default rate for investment-grade CLOs (AAA to BBB) between 1996-2023 was less than 0.1%, or 19 instances across nearly 23,000 tranches.

Since 2010, in large part to various structural improvements such as more senior loan portfolios, a shorter reinvestment period, and more par subordination, no S&P-rated investment-grade CLO has defaulted9.

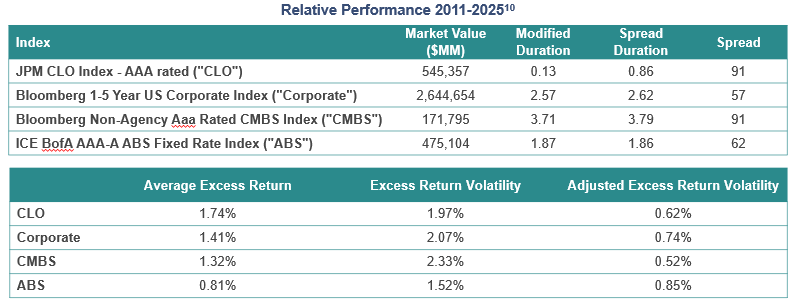

What is historical performance for AAA CLOs compared to other short-duration fixed income segments?

The table below details characteristics of AAA-rated CLOs and other comparable fixed income segments based on representative index data. Modified duration is a measure of the sensitivity of a bond’s price to a given change in interest rates. Spread duration is a measure of the sensitivity of a bond’s price to a given change in its credit spread. As a floating rate asset class, CLOs have little modified duration by definition, as the coupons will adjust higher or lower with changes in Term SOFR. CLOs currently also exhibit relatively low spread duration while providing competitive spreads relative to other short-duration segments.

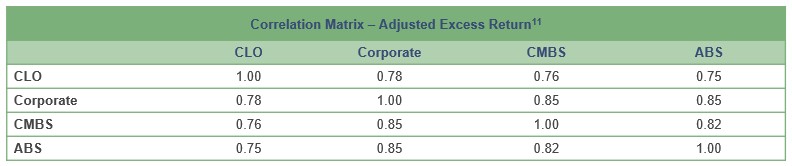

CLOs also demonstrate favorable excess return correlations, even after standardizing the metric by spread duration. For eligible portfolios, AAA CLOs’ lower historical correlation profile relative to the sectors shown below offers the potential for increased risk-adjusted returns, in our view.

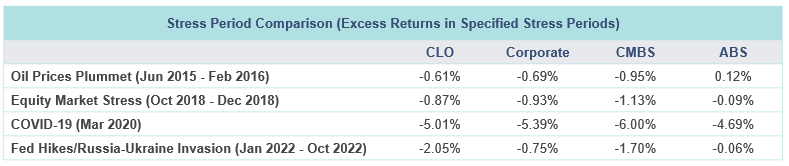

How do AAA CLOs perform in adverse market environments?

Floating-rate AAA CLO excess returns in periods of recent stress are comparable to short-duration, fixed-rate sectors. AAA CLOs outperformed corporate bonds and CMBS in three of the four scenarios shown, though notably were the worst performer in 2022. ABS was consistently the best performer in the stress periods shown.

About the Author

James Kerin, CFA®, Director, joined SCM in 2020 and has investment experience since 2013. James is a Fixed Income Portfolio Manager on SCM's Fixed Income Team. Prior to joining SCM, he was an associate analyst at Moody’s Investors Service. James received his B.A. from the University of Dallas. He holds the Chartered Financial Analyst® designation.

Related Insights

03.11.2026 • Charles Wittmann, CFA®

02.11.2026 • Charles Wittmann, CFA®

01.13.2026 • Charles Wittmann, CFA®

12.11.2025 • Charles Wittmann, CFA®