Overview

Energy prepayment (prepay) bonds enable municipal utilities to lock into a discounted price on a long-term supply of energy, most commonly natural gas or electricity. Issued by special purpose authorities, bonds are structured with far-dated final maturities but shorter-dated mandatory tenders that are backed by the obligation of a bank or insurance company, known as the guarantor, to ensure that it occurs in order to return principal to bondholders. As a result, prepay bonds are ultimately a corporate credit exposure in the tax- exempt market. The final maturity matches the term of the energy supply contract and improves the bond’s market discount tax treatment, while the shorter-dated tender serves to optimize borrowing costs within the transaction.

History

Prepay bonds were first issued in the 1990s. The original natural-gas-oriented transactions were scrutinized by the Internal Revenue Service (IRS) for potential misuse of tax-exempt proceeds for investment returns or private business use rather than for governmental purposes, as tax-exempt status is only available to bonds that pass various IRS tests both at issuance and throughout their life cycle.1

In 2003, the IRS implemented enhanced regulations outlining the specific circumstances required to justify the tax-exemption, such as at least 90% of the energy being provided to retail customers in the service area of the municipal utility. In 2005, U.S. Congress subsequently passed the Energy Policy Act, which wrote a modified version of the prior IRS action into the tax code, providing additional clarity to the market. Historically, prepay bonds reflect the low default characteristics of the overall municipal market with only one default stemming from the 2008 Lehman Brothers collapse.2

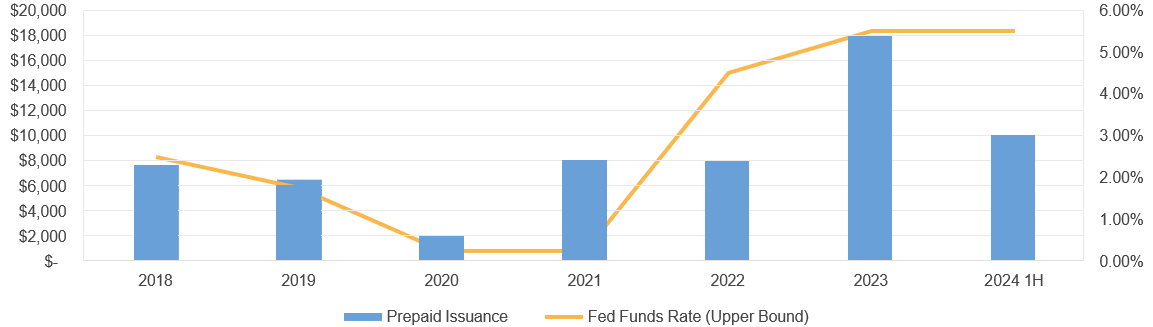

Since the Great Financial Crisis of 2007-2008, volumes of prepay bond issuance have significantly fluctuated year-to-year. The primary driver for issuance is the difference between the tax-exempt and taxable yields, which tends to occur in higher interest rate regimes (when the Fed Funds Rate is raised, per the chart below). From the perspective of the bank or insurance company guarantor, the difference between the tax-exempt yield and the yield on its alternative taxable funding source is considered “savings,” as it represents a lower cost of funding and more potential profit. These savings can be shared with the participating municipal utilities in the form of a discount on energy.

Transaction Structure

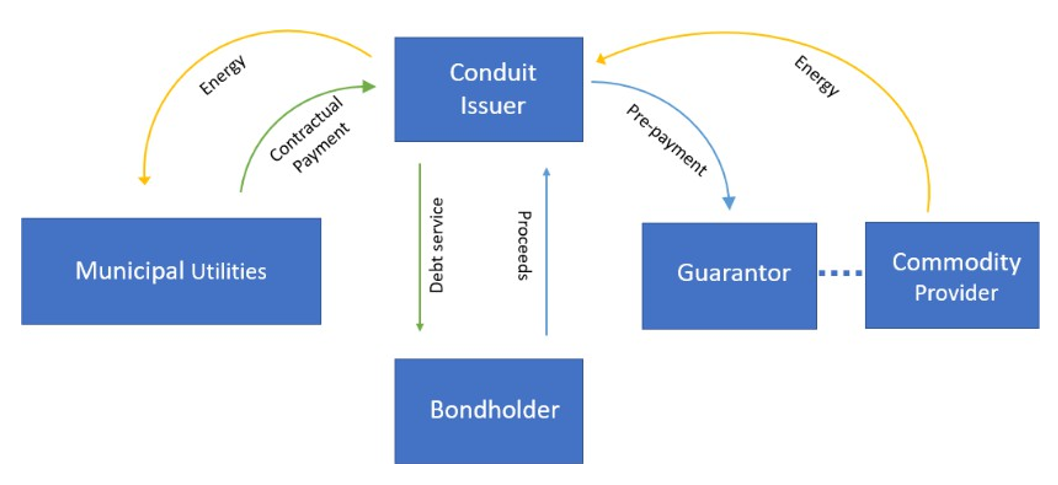

To initiate the transaction, prepay bonds are issued by the conduit issuer and proceeds fund the prepayment for energy on behalf of participating utilities. The payment is invariably quite large, as it represents large quantities of energy over a 20- to 30-year period. The payment flows to the guarantor backing the transaction.

In exchange for accepting the prepayment, the guarantor must provide for the supply of energy to the utilities, either directly through its subsidiary commodity trading business or indirectly via supply contracts with an energy company. Prepay guarantors are typically investment-grade banks or insurance companies who are well positioned to handle the complexity of the deal’s asset-liability matching characteristics and associated cash-flows.

As the municipal utilities receive the energy over time in agreed upon quantities and locations, they make periodic payments to the issuer of the bonds per the terms of outstanding energy purchase agreements. These payments, based on an energy index price less the contractual discount, provide the source of funds for debt service payments, retiring principal, and funding coupon payments to bondholders.

Commodity Swaps

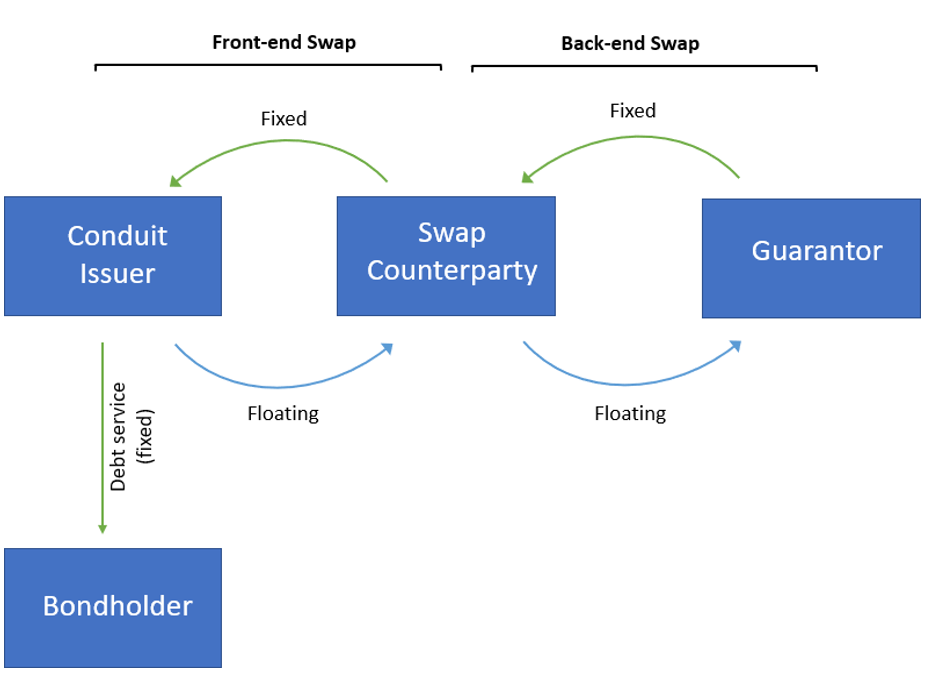

As debt service on the prepay bonds is fixed but the contractual payment from the municipal utility is variable, a commodity swap must be embedded within the transaction to eliminate market price risk. Without the swap, it is possible for the market-based payment from the utility to fall below the required level to fund debt service simply due to price volatility in the underlying commodity.

First, a commodity swap is entered in between the issuer and a counterparty, where the issuer passes on the floating-rate payment that it received from the utilities and receives a fixed-rate payment from the counterparty. This contract, referred to as the front-end swap, effectively removes market price risk from the transaction but also creates counterparty risk, as the swap’s fixed rate payment is now used to fund debt service.

To structurally transfer this risk from the counterparty to the guarantor, a back-end swap is also created with matching offsets of notional energy quantities and delivery points relative to the front-end swap. The counterparty is consistent in both swap agreements, though the parties involved change to the counterparty and the deal’s guarantor. Here, the guarantor pays a fixed-rate payment and receives a floating-rate payment. With the swap agreements overlaid upon one another, the swap counterparty becomes an administrative entity that passes payments between the conduit issuer and the guarantor rather than an additional source of credit risk.

Importantly, if the counterparty fails to make the fixed payment in the front-end swap, the fixed payment from the guarantor in the back-end swap can be utilized in its stead via a custodial agreement. The governing documents allow for the replacement of the swap counterparty within 120 days; if the counterparty cannot be replaced, the energy purchase agreement terminates and the guarantor returns principal to the bondholders.

Benefits

Guarantor: participating in prepay bonds may provide an attractive cost of capital for the guarantor relative to alternative funding sources, as yields for the tax-exempt bonds are lower than the yields on their taxable bonds. Bond proceeds may be utilized at the guarantor’s discretion, including for its operations, such as making loans or investments. Additionally, if the guarantor has a commodity trading subsidiary, it can leverage its existing expertise to generate additional revenue in that business.

Municipal utilities: participating in prepay bonds presents an opportunity for utilities to lock into a long-term discount on market prices, allowing utilities to operate more efficiently. For smaller, rural utilities with limited access to the capital markets, participating in an energy prepayment bond alongside other utilities can be appealing financially. Utilities may also look to prepay bonds when striving to meet external or internal renewable energy targets, as the transaction places project responsibility on industry specialists. Finally, the debt is non-recourse to utilities, meaning that investors may only look to the guarantor for remedies if the underlying utilities are unable to take-or-pay for the energy. This is an additional benefit, in our view, as prepay deals do not impact utility credit quality with rating agencies.

Bondholders: funding the prepayment to the energy supplier may be advantageous for investors as the bonds have strong credit fundamentals with attractive spreads in diversifying names. Relative to more traditional A- and BBB-rated revenue bond municipal credit, investors can pick up spread and boost portfolio yields, reflective of the corporate credit risk of the guarantor. In many cases, the yield of the tax-exempt prepaid bond is greater than the yield on the guarantor’s taxable bonds on an after-tax basis.

Risks

No two deals are the same, but universally, the credit quality of the bonds is based on the ability and willingness of the guarantor to backstop the transaction in various key situations.

The guarantor pledges it will fund an extraordinary redemption payment for the bonds if there is a failed remarketing at the tender date (the effective maturity date), the timing of which is known far in advance. In addition, the guarantor commits to funding a termination payment to unwind the transaction and return principal to bondholders if the energy purchase agreement is terminated.

Sterling Capital Management participates in energy prepayment bonds with only the highest quality guarantors to benefit from strong credit quality and enhanced liquidity. We believe that these bonds are additive to eligible client accounts due to the sector’s attractive yields and satisfactory structural fundamentals.

About the Authors

James Kerin, CFA®, Director, joined SCM in 2020 and has investment experience since 2013. James is a Fixed Income Portfolio Manager on SCM's Fixed Income Team. Prior to joining SCM, he was an associate analyst at Moody’s Investors Service. James received his B.A. from the University of Dallas. He holds the Chartered Financial Analyst® designation.

Michael McVicker, Executive Director, joined SCM in 1992 and has investment experience since 1992. Mike is Head of Municipal Credit Analysis and responsible for portfolio management of enhanced cash and short-intermediate municipal portfolios, as well as Associate Portfolio Manager responsibilities for the state-specific municipal bond portfolios for the Sterling Capital Funds. Prior to joining the Fixed Income team, he was SCM's Director of Operations managing the client reporting and performance team. Mike received his B.S.B.A. in Finance with a minor in Psychology from the University of North Carolina at Charlotte.

Related Insights

03.28.2025 • James Kerin, CFA®

01.27.2025 • Andrew Richman, CTFA

Meet Andrew Richman, Sterling Capital Managing Director and Senior Fixed Income Client Strategist

12.12.2024 • Orton Chen, CFA®

Meet Orton Chen, Chief Investment Officer for Sterling Capital's Private Client Group

11.22.2024 • Shane Burke

Meet Shane Burke, Sterling Capital Advisory Solutions Portfolio Manager

Explore