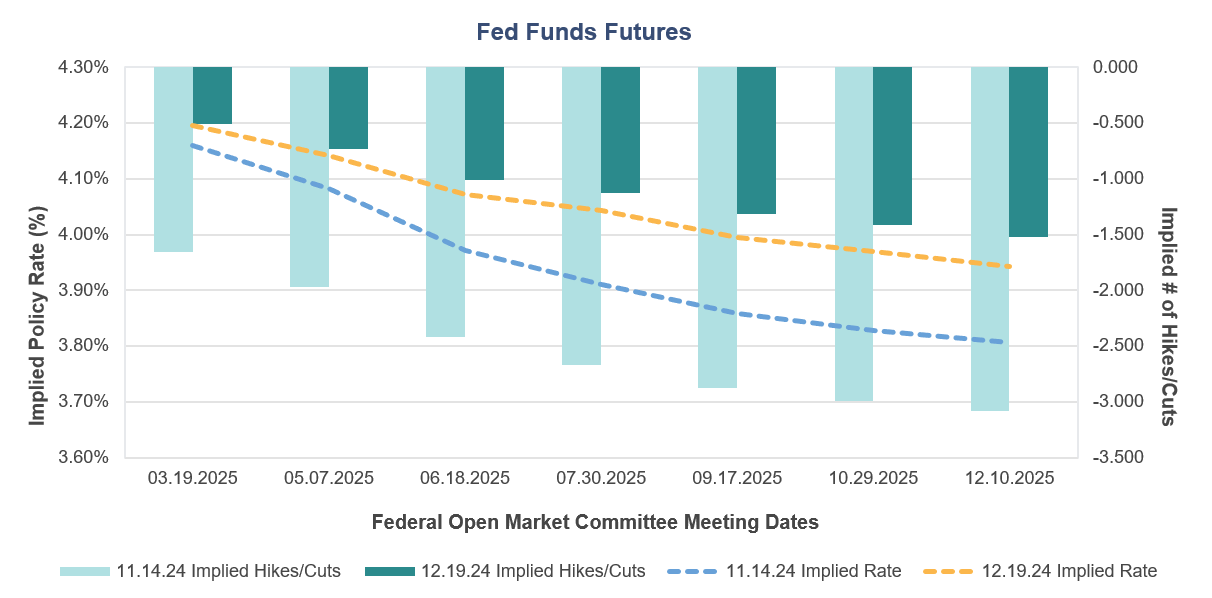

The Federal Reserve (Fed) lowered rates by another 25 basis points (bps) this week, bringing the total reduction to 100 bps or a full 1.0% since they began in September. This leaves the fed funds rate at a range of 4.25% to 4.50%. Notably, there was one dissenter who preferred to maintain the target rate. This was widely expected but the market’s reaction was more forward looking and focused on the Fed’s updated Summary of Economic Projections. The Fed raised their forecasts for both growth and inflation. Real gross domestic product (GDP) is now forecasted to come in at 2.50% for this year and 2.10% for 2025. On the inflationary front, the Fed’s median forecast for the Core Personal Consumption Expenditures Index (PCE) rose to 2.80% this year and 2.50% for 2025. In fact, their forecast now calls for inflation to remain and 2.0% goal, through 2026. Finally, unemployment was revised down.

These revised-higher economic projections in Federal Open Market Committee (FOMC) forecasts resulted in the market swiftly re-pricing future Fed rate cuts and U.S. Treasury yields precipitously rising. The long end was particularly vulnerable as the ten-year and thirty-year bond yields rose by approximately 13 bps, which resulted in a steepening of the curve. The market and the Fed now only expect two additional fed funds rate cuts through 2025.

In the press conference after the rate decision, Fed Chair Jerome Powell mentioned their dual mandate when he referenced the risks to achieving employment and inflation goals as being roughly in balance. He went on to state that policy has been moving toward a more neutral setting. Additionally, while answering questions, Powell mentioned the decision was paired with the extent and timing language in the post meeting statement that signals we are at or near a point that it will be appropriate to slow the pace of further adjustments. This appears to suggest that a pause in rate cuts is nearing.

About the Author

Andrew Richman, CTFA, Managing Director, joined SunTrust in 2001 and SCM in 2020 as part of an integration following the merger of equals between SunTrust Banks and BB&T Corporation. Andy has investment experience since 1988 and is a Fixed Income Portfolio Manager and Senior Fixed Income Client Strategist. Prior to his 20 years in SunTrust’s portfolio management division, Andy ran a trust and investment department in Florida as the trust department senior manager and worked as an equity portfolio manager with Sanford Bernstein. He received his B.A. from the State University of New York at Albany and his M.B.A. with a concentration in International Business from the University of Miami. He is also a graduate of the ABA National Trust School at Northwestern University and holds the Certified Trust & Financial Advisor designation.

Related Insights

10.30.2025 • Andrew Richman, CTFA

Fed Cuts Rates Again, But Additional Cuts Are Not Guaranteed

10.23.2025 • Charles Wittmann, CFA®

10.03.2025 • Michael McVicker

09.24.2025 • Tom O'Toole

Explore