The proliferation of benchmark tracking funds in the investment world has led to one large misnomer: passive investing. While definitions vary, the most common form of passive investing is purchasing a fund that mimics an underlying index and holding for longer time horizons. It is easy to see how the word passive can become conflated with static or stable allocations. However, if the asset itself changes materially over time, how passive is it really?

To illustrate the point, look no further than one of the largest and most commonly used benchmarks in the fixed income space - the Bloomberg U.S. Aggregate Bond Index. Consider a scenario in which an investor purchased an exchange-traded fund (ETF) that simply mimics the characteristics of this index (i.e., a passively managed ETF) in 2005, this ETF is the investor’s only holding, and for 20 years the investor does not adjust their holdings. Does the risk profile of the investor’s portfolio change over time?

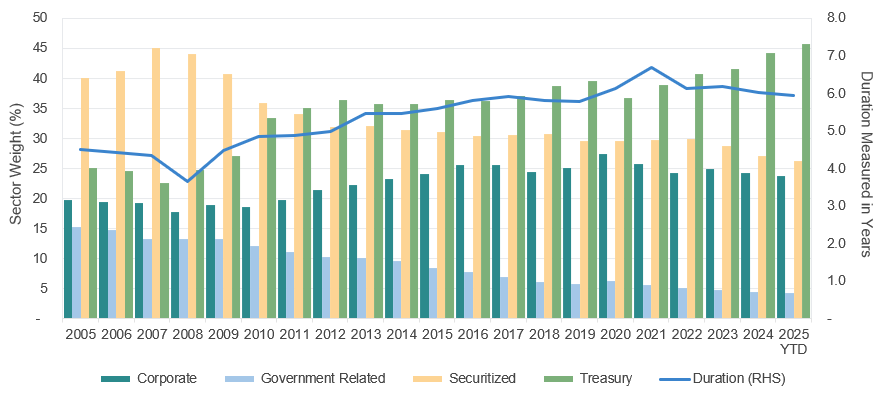

On the surface, our investor has maintained 100% passive exposure to the U.S. fixed income market. While the passive allocation has been constant, the market index it tracks has been anything but. Since it is a rules-based index, any bond that meets the inclusion criteria is added to the universe, and as sector issuance ebbs and flows, the asset allocation mix and characteristics of the index reflect those changes over time. Comparing the index changes over the holding period highlights just how much the “passive” investments have shifted.

Without touching anything, the asset allocation mix of the underlying holdings changed meaningfully over the years. The portfolio’s drift is not contained to just asset allocation as the characteristics of the index it mimics have also changed over time. In simplistic terms, a bond or portfolio’s duration is a measurement of price sensitivity to changes in interest rates. In 2005, the option adjusted duration of the Bloomberg U.S. Aggregate Bond Index was 4.16. By 2025, the duration lengthened substantially to 6.06, making the portfolio more sensitive to interest rate moves, again without the account lifting a finger!

Passive investing may seem simple, but it carries hidden risks. As market conditions change, a passive fund’s risk profile can shift without investors realizing it, leading to unintended exposures. Active management, by contrast, continuously monitors and adjusts to mitigate these risks. In fixed income, where risk is inherently asymmetric, understanding risk exposures on a standalone basis and in relation to other holdings is critical to avoid unintended risks and ultimately protect the end investor.

About the Authors

Gregory Zage, CFA®, Executive Director, joined SCM in 2007 and has investment experience since 2007. Gregory is a Senior Fixed Income Portfolio Manager and Head of Fixed Income Trading. He is currently responsible for all trading activity across SCM's fixed income desks. Previously at SCM, he was responsible for high-grade corporate credit trading and municipal credit trading. Gregory received his B.A. in Economics with a minor in Spanish from Davidson College. He holds the Chartered Financial Analyst® designation.

Justin Nicholson, Director, joined BB&T Asset Management in 2002 and SCM through merger in 2010. He has investment experience since 2002. Justin is a Fixed Income SMA Portfolio Manager. Justin received his B.S. in Business Management from North Carolina State University.

Related Insights

03.11.2026 • Charles Wittmann, CFA®

02.11.2026 • Charles Wittmann, CFA®

01.13.2026 • Charles Wittmann, CFA®

12.11.2025 • Charles Wittmann, CFA®