Long-term bond yields reflect the weighted path of the fed funds rate as determined by the Federal Reserve (Fed) plus a term premium. What is term premium and why is it important?

Definition

Put simply, term premium is the additional return investors demand for holding a longer-term bond instead of buying and reinvesting a series of short-term bonds over the same time period. This additional expected return compensates investors for interest rate risk, inflation uncertainty, and market liquidity preferences, among other factors, and is an important determinant of the shape of the yield curve.

Term premium is not directly observable or measurable, but it can be estimated with statistical methods that decompose yields into discrete factors. We favor the Adrian, Crump, and Moench (ACM) 10-year Treasury Term Premium model (ACMTP10)1 as it was created by researchers at the New York Fed and benefits from its more simplistic, straightforward approach relative to other techniques. Of note, measures of term premium can vary significantly by hundreds of basis points, so viewing various estimates of term premium together can be worthwhile.

Historical Review

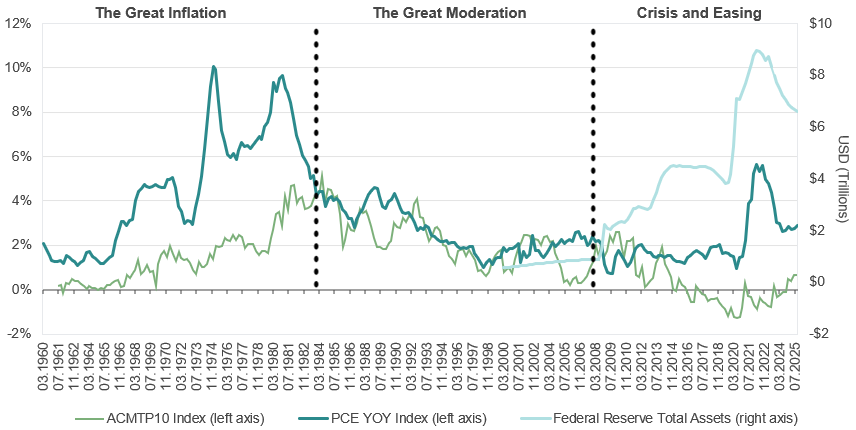

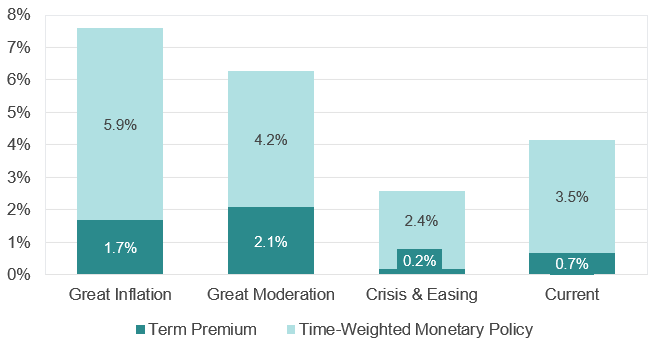

Term premium has demonstrated a relatively slow rate of change over time as investors gradually distinguish between one-time events and structural shifts. In the 1960s-1970s, as it became apparent that inflation was entrenched, investors demanded additional compensation to hold long-term bonds. As a result, term premium rose in fits and starts from effectively zero to >4% over a 20-year period.

1According to the Federal Reserve, New York Fed economists Tobias Adrian, Richard K. Crump, and Emanuel Moench developed a dynamic no-arbitrage linear term structure model to describe the joint evolution of Treasury yields and term premia across time and maturities, described in detail in Adrian, Crump, and Moench (2013). In these models, bond yields are driven by a small number of 'pricing factors' – which are linear combinations of yields, such as principal components – and which evolve over time according to a vector autoregressive (VAR) process.

In the 1980s and 1990s, inflationary pressures eased as globalization and information/communication technology transformed the economy. Real growth surged and culminated in a fiscal surplus for the U.S. government in 2001 as they benefitted from strong demographic trends and productivity gains. Against this backdrop, general uncertainty fell, and term premium followed suit.

Following the Great Financial Crisis (GFC) in 2008 and the pandemic in 2020, the Fed notably expanded its balance sheet to support the financial system via quantitative easing (QE). During this time, term premium further retreated, even going deeply negative, as the Fed moved from being a marginal participant in the Treasury market to owning over $4T in U.S. Treasury bills, notes, and bonds today. The Fed’s actions simultaneously skewed the supply/demand dynamics of the market and lowered the perceived risk of holding longer-term bonds, reducing the term premium demanded by the market.

Present Day

Today, positive term premium is on the rise as the Fed reduces its balance sheet via quantitative tightening (QT) and broad-based inflationary pressures have increased. Should the term premium remain close to zero?

No. We believe term premium should be higher, but with caveats.

With inflation around 3% (as measured by core PCE) and tariff pressures threatening, the Fed has resumed cutting the fed funds rate after pausing for nearly a year to proactively manage downside risks to the labor market. Both monetary policy and economic uncertainty are likely rising in this environment.

Offsetting that uncertainty, however, is the Fed’s role as a permanent holder of U.S. Treasury instruments. The Fed expects to end QT in the near future and ultimately begin increasing the size of its balance sheet. Meanwhile, the Treasury Department has increased its T-bill issuance to above historical average levels, thereby reducing the amount of longer-dated duration the market must absorb. These actions suppress term premium. The Trump administration is focused on lowering the 10-year yield, putting a higher-term premium at direct odds with their policy aims, in our view. Accordingly, while long-term rates remain predominantly market-driven, the influence of policy actions on rates is structurally increasing, and term premium is unlikely to reach prior highs.

About the Author

James Kerin, CFA®, Director, joined SCM in 2020 and has investment experience since 2013. James is a Fixed Income Portfolio Manager on SCM's Fixed Income Team. Prior to joining SCM, he was an associate analyst at Moody’s Investors Service. James received his B.A. from the University of Dallas. He holds the Chartered Financial Analyst® designation.

Related Insights

03.11.2026 • Charles Wittmann, CFA®

02.11.2026 • Charles Wittmann, CFA®

01.13.2026 • Charles Wittmann, CFA®

12.11.2025 • Charles Wittmann, CFA®