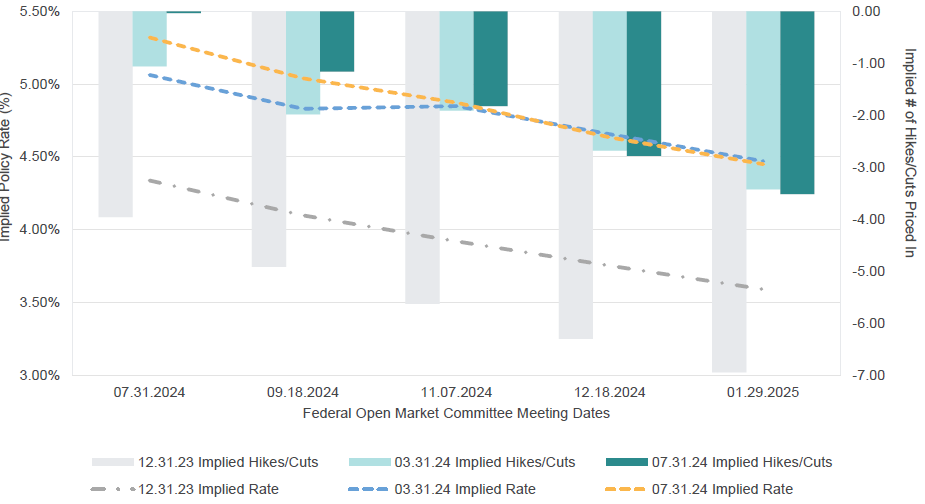

The Fed kept rates unchanged as expected after yesterday’s meeting but signaled a rate cut in September is clearly in play. From the FOMC statement, “The committee judges that the risks to achieving its employment and inflation goals continue to move into better balance.” During the press conference that followed Fed Chair Jerome Powell was more direct in regard to future rate cuts, “…reduction in the policy rate could be on the table as soon as the next meeting in September.” Powell did emphasize that they would weigh incoming data, and no cuts or several are still on the table for next year, but we believe it is reasonable to presume that a cut(s) was discussed during this meeting.

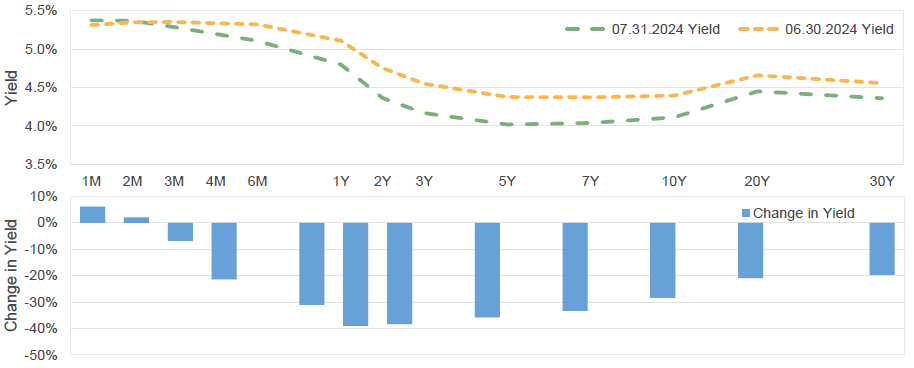

Bonds continued to rally as the yield on the U.S. 10-Year Note approached 4.00%. The yield closed at 4.04%, down 35 basis points (bps) for the month. The front end of the curve also rallied, with the two-year yield at 4.27%, down a whopping 48 bps over the last 30 days. These moves resulted in a less inverted curve. In fact, the slope of the two-year U.S. Treasury Note to 30-year is now positive after being negative for over a year.

The market is anticipating a more normalized curve as inflation moderates, growth slows, and the Fed begins to ease. The market is now pricing in two full cuts for the remainder of 2024 and another four in 2025. This would result in a Fed Funds effective rate of approximately 3.50% by December 2025.

About the Author

Andrew Richman, CTFA, Managing Director, joined SunTrust in 2001 and SCM in 2020 as part of an integration following the merger of equals between SunTrust Banks and BB&T Corporation. Andy has investment experience since 1988 and is a Fixed Income Portfolio Manager and Senior Fixed Income Client Strategist. Prior to his 20 years in SunTrust’s portfolio management division, Andy ran a trust and investment department in Florida as the trust department senior manager and worked as an equity portfolio manager with Sanford Bernstein. He received his B.A. from the State University of New York at Albany and his M.B.A. with a concentration in International Business from the University of Miami. He is also a graduate of the ABA National Trust School at Northwestern University and holds the Certified Trust & Financial Advisor designation.

Related Insights

07.02.2025 • Charles Wittmann, CFA®

06.20.2025 • Andrew Richman, CTFA

06.10.2025 • Charles Wittmann, CFA®

05.07.2025 • Charles Wittmann, CFA®

Explore