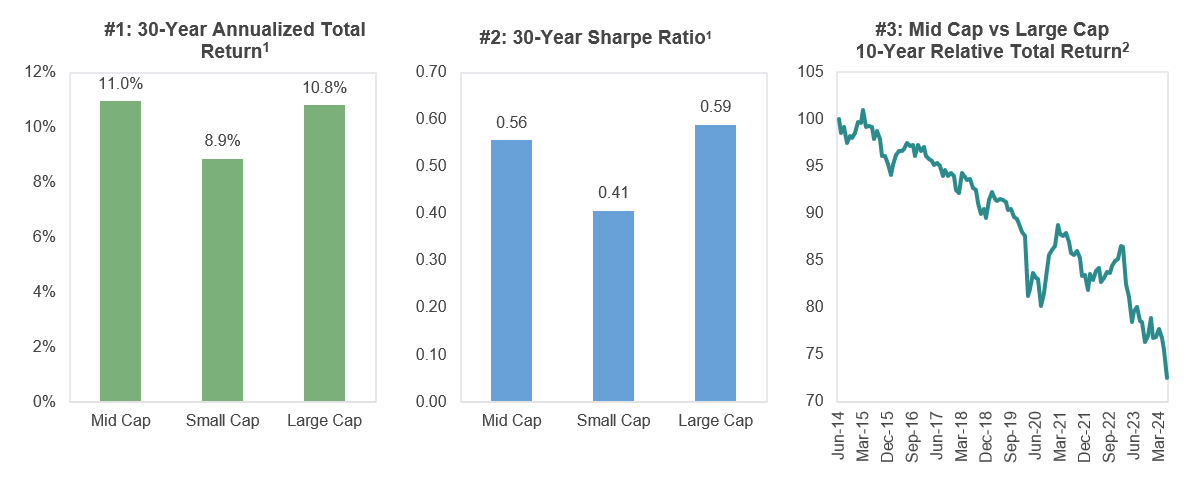

For almost a decade, large-cap growth has been a dominant factor driving market returns. However, we see mounting evidence mid-cap value stocks are due for a comeback. We have long argued mid caps are a potential “sweet spot” for investors. We believe they boast better liquidity, stronger balance sheets, and more durable competitive advantages than small-cap peers and are often more nimble, focused, and less well covered by the sell side than large caps. This combination has led to strong risk-adjusted returns. Below we show the thirty-year annualized returns for large, mid, and small caps measured by the Russell 1000® Index, Russell MidCap® Index, and Russell 2000® Index, respectively (Chart #1). For total return, mid caps have edged out large caps and comfortably beaten small caps all with favorable risk-adjusted metrics (Chart #2). Mid cap’s long-term performance is notable, as it includes the sharp underperformance relative to large caps over the last decade (Chart #3). With that as today’s setup, we believe it is a good time to revisit the category.

We attribute much of mid cap’s recent underperformance to the anomalous concentration in market returns. The S&P 500® Index has returned +14.5% through 2Q24, but 57% has come from five stocks: Nvidia, Alphabet, Microsoft, Meta and Amazon. Nvidia alone has contributed 30%, the largest by a single stock in over a century. This echoes last year when those same five companies accounted for almost half the index’s return. To put this in context, there have only been nine instances where five stocks or fewer have contributed at least 40% of market returns in the last sixty years. We just experienced two back-to-back.

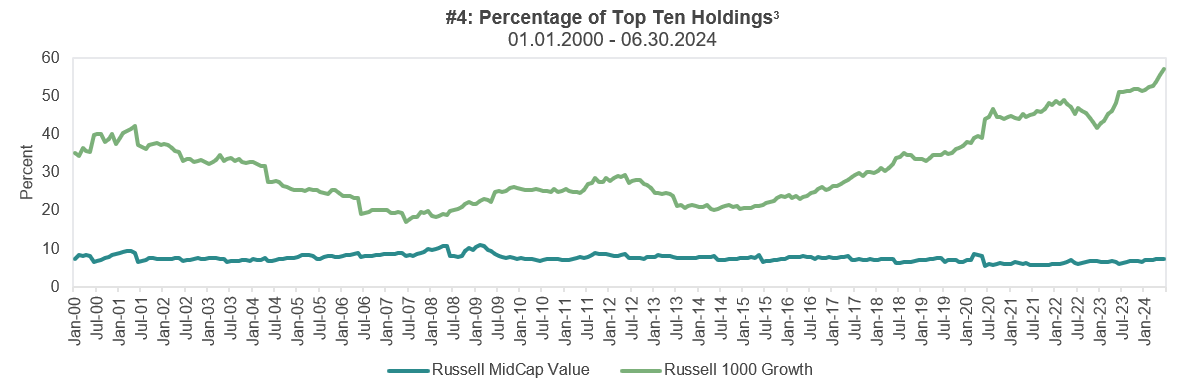

This ever-increasing concentration is now spilling into index construction. Russell reconstitutes its benchmarks each June, and we believe there are some noteworthy stats this year. The top ten holdings of the Russell 1000® Growth Index now account for 60% of the index (Chart #4), the highest concentration ever. The Russell Midcap® Growth Index only has 288 constituents, the fewest ever. Meanwhile the Russell Midcap® Value Index boasts 713 holdings, roughly in-line with history, and the top ten account for 7.4%, slightly below the historic average of 7.6%.

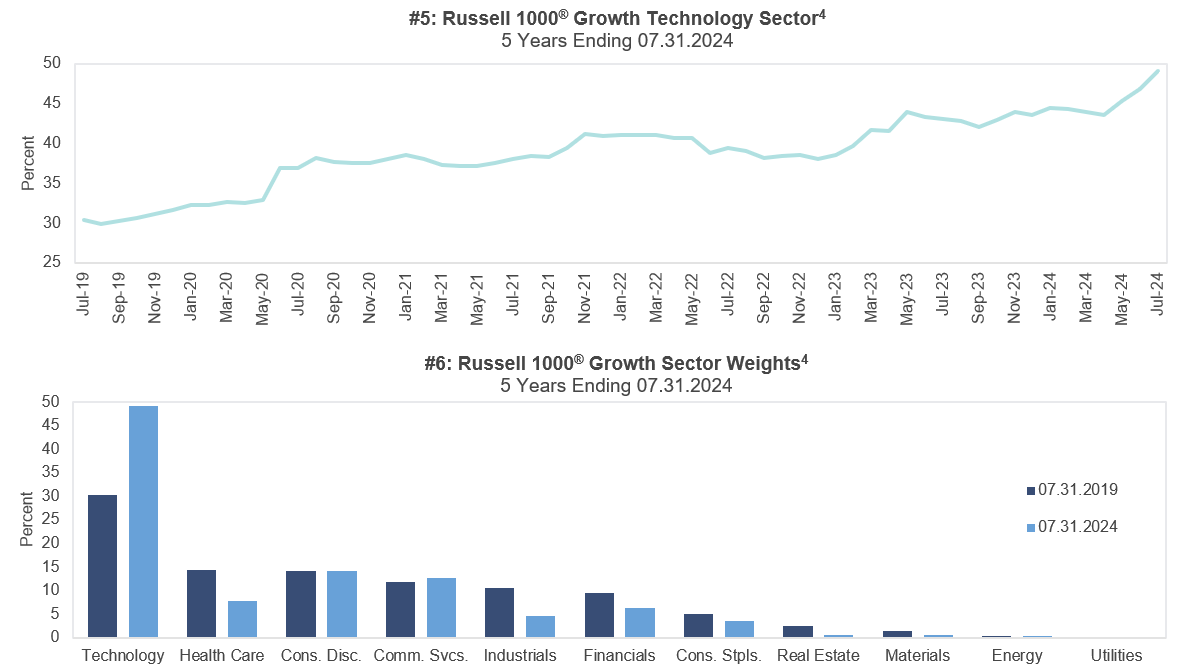

An analysis at the sector level (Chart #5, #6) highlights even greater disparities. The Russell 1000® Growth now has a 50% weighting to technology, the highest ever, and more than 5x higher than its value equivalent, the Russell 1000® Value. Concentration is now so high that many indices would run afoul of the requirements to be considered diversified funds stipulated in the Investment Company Act of 1940. We see this as a risk for allocators and one that may be reduced by revisiting mid-cap value where concentration remains in line or below history.

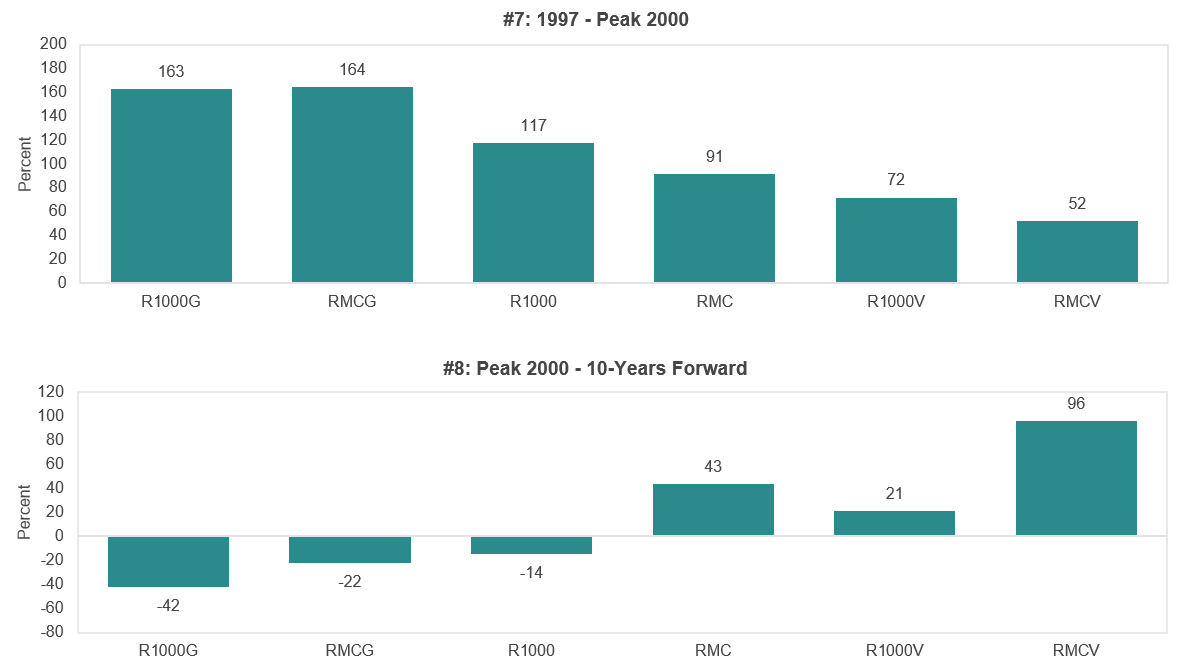

History provides some context regarding whether large-cap growth can continue to dominate forward returns. Investors saw a similar scenario in the run up to the dot-com bubble where large-cap growth stocks trounced their mid-cap value peers (Chart #7). However, once the bubble burst, mid caps delivered a decade of solid performance. The Russell Midcap® Value nearly doubled while the Russell 1000® Growth declined a cumulative 42% (Chart #8). We argue the starting point looks similar today given the magnitude of large cap’s overperformance over the last ten years and the current enthusiasm for technology stocks.

In conclusion, we are optimistic on mid caps given their history of strong returns and attractive risk metrics. It is always difficult to call the peak of a cycle, however we believe the current setup is favorable. Today’s unprecedented concentration suggests the spring is coiled tightly should a recovery materialize. For almost twenty years our strategy has aimed to own good businesses with good management at a good price. We are hopeful these attributes will prove favorable as the breadth of the market widens in time.

About the Author

Will Smith, CFA®, Executive Director, joined SCM in 2015 and has investment experience since 2002. Will is the Portfolio Manager of the Fundamental Equity Mid Cap Value strategy. Prior to joining SCM, he was an executive director with Goldman Sachs in London as the lead sell side analyst covering the global media and telecommunications sector. Prior to Goldman Sachs, he worked for Jefferies International as the lead sell side analyst covering the global media sector. Will received his B.E. in Structural Engineering from Vanderbilt University and his M.B.A. from the London Business School. He holds the Chartered Financial Analyst® designation.

Related Insights

07.02.2025 • Charles Wittmann, CFA®

06.20.2025 • Andrew Richman, CTFA

06.10.2025 • Charles Wittmann, CFA®

05.07.2025 • Charles Wittmann, CFA®

Explore