The fourth quarter of 2024 started with a bang but ended in a whimper for the market, in our view. One of the most interesting dynamics to us was the relative underperformance of value stocks compared to the overall market and the nature of the performance. For context, the Russell 1000® Value Index was down -2.0% on a total return basis while the S&P 500® Index was up +2.4%.

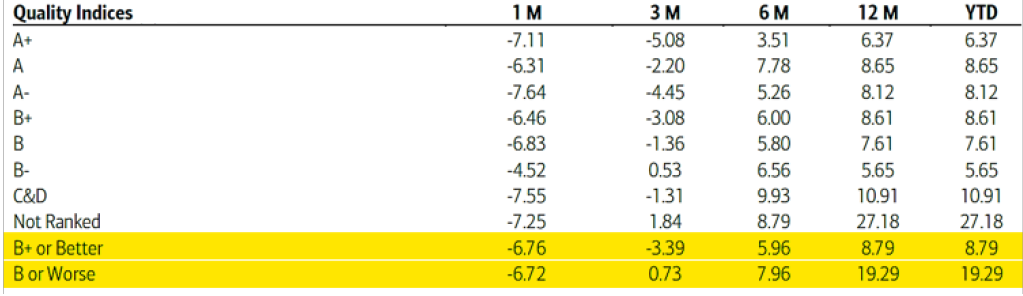

We believe the other interesting component was the nature of what stocks worked in both indices. The table above shows the performance in 4Q24 and 2024 for stocks based on S&P quality measures that include return on equity (ROE) and balance sheet leverage, with higher-quality stocks receiving higher letter grades. The table shows in the bottom two lines how low-quality stocks with B or worse ratings outperformed higher-quality stocks of B+ or better by +4.12% for the quarter and +10.50% for the year.

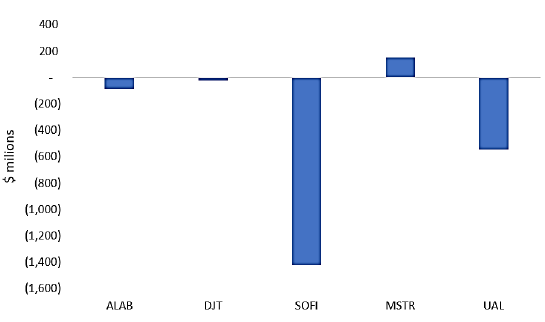

This dynamic appears to be confirmed by the top five absolute performers in the Russell 1000 Value during the quarter, seen in the chart to the right. Over the past three calendar years, this group of stocks earned a profit in only 20% of those years.

Only the cryptocurrency-focused stock, Microstrategy, generated a profit, while cumulatively they lost money over those years. With unprofitable companies constituting the top performers in the Russell 1000 Value, we believe it provides confirmation for the Bank of America Global research that low-quality stocks performed well in the most recent quarter.

2021-2023

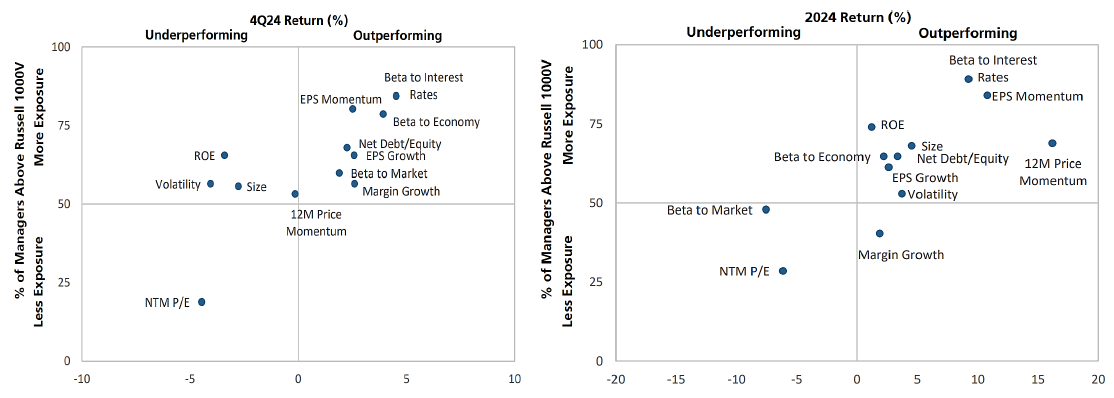

Large Cap Value Peer Group

On the charts above, we show what worked in the large cap value space relative to the peer group rather than the index. These charts for Q4 and 2024 appear to show a similar story. What worked in the upper right quadrant was momentum, whether it was price or earnings, managers willing to own stocks with risk related to interest rates, the macroeconomy, or higher balance sheet leverage.

While quarter-to-quarter and occasionally year-to-year certain characteristics may come in and out of favor, we have found that our focus on quality companies with strong balance sheets, earnings growth, and attractive valuations may position clients for success in the long term.

As always, thank you for your interest and trust managing your investments.

About the Author

Charles Wittmann, CFA®, Executive Director, joined SCM in 2014 and has investment experience since 1995. Chip is Co-Portfolio Manager of the Equity Income strategy. Prior to joining SCM, he worked for Thompson Siegel & Walmsley as a portfolio manager and (generalist) analyst. Prior to TS&W, he was a founding portfolio manager and analyst with Shockoe Capital, an equity long/short hedge fund. Chip received his B.A. in Economics from Davidson College and his M.B.A. from Duke University's Fuqua School of Business. He holds the Chartered Financial Analyst® designation and served as President of CFA Society Virginia from 2012-2013.

Related Insights

11.11.2025 • Charles Wittmann, CFA®

10.30.2025 • Andrew Richman, CTFA

Fed Cuts Rates Again, But Additional Cuts Are Not Guaranteed

10.23.2025 • Charles Wittmann, CFA®

10.03.2025 • Michael McVicker

Explore