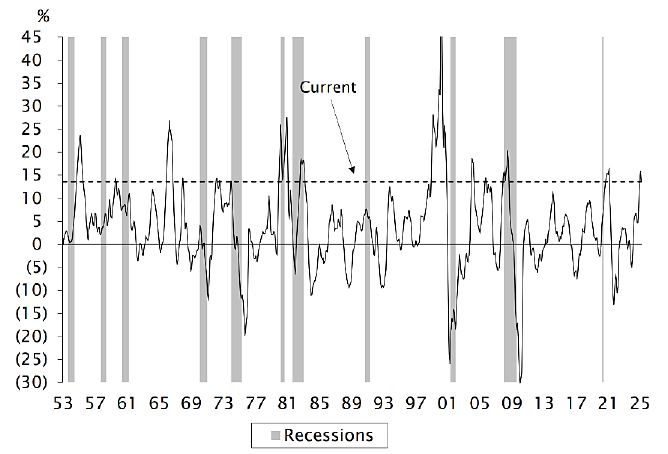

Trailing 12-Month Returns (1953 - February 2025)

This month, we’re happy to share some market dynamics that we observed anecdotally but now have facts and figures to support. For the past two years, investors have experienced a powerful momentum-driven market. In investing, momentum is like a train – once it gets started, it is propelled in the same direction. Momentum investing capitalizes on our herding behavior when investors choose upward-trending stock prices and believe they will continue. Many times they will combine signals, such as when analysts who publish earnings estimates on these companies’ stocks revise their earnings forecasts upward to help verify the upward direction of a stock.

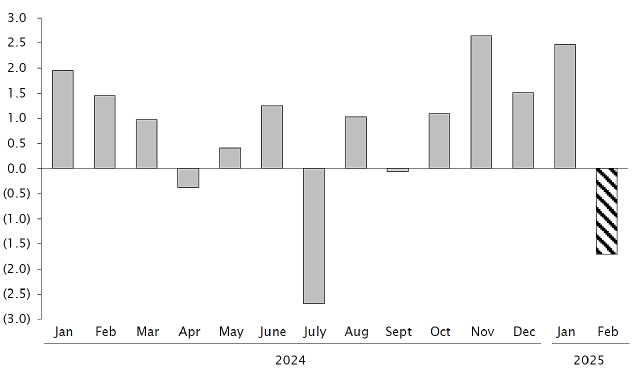

In terms of price momentum, we can see from the Empirical Research chart at the top of the page that over the last 12 months, price momentum has had one of the best performance periods in seventy years. Earnings revisions tend to have short performance signals, but we believe there is a common thread between price momentum and earnings momentum, as seen in the chart to the right. It shows that stocks that have seen their earnings estimates revised upward have consistently outperformed over the following month.

Typically, this type of tight relationship is seen coming out of a recession. We believe the 50 basis point (bp) fed funds rate cut last year (the first this century outside of a major crisis such as the housing crisis, Global Financial Crisis, or COVID-19) contributed to this differentiated dynamic in late 2024.

2024 - February 2025

This past month has been challenging for momentum stocks and earnings revisions as the bar for earnings revisions has been raised.

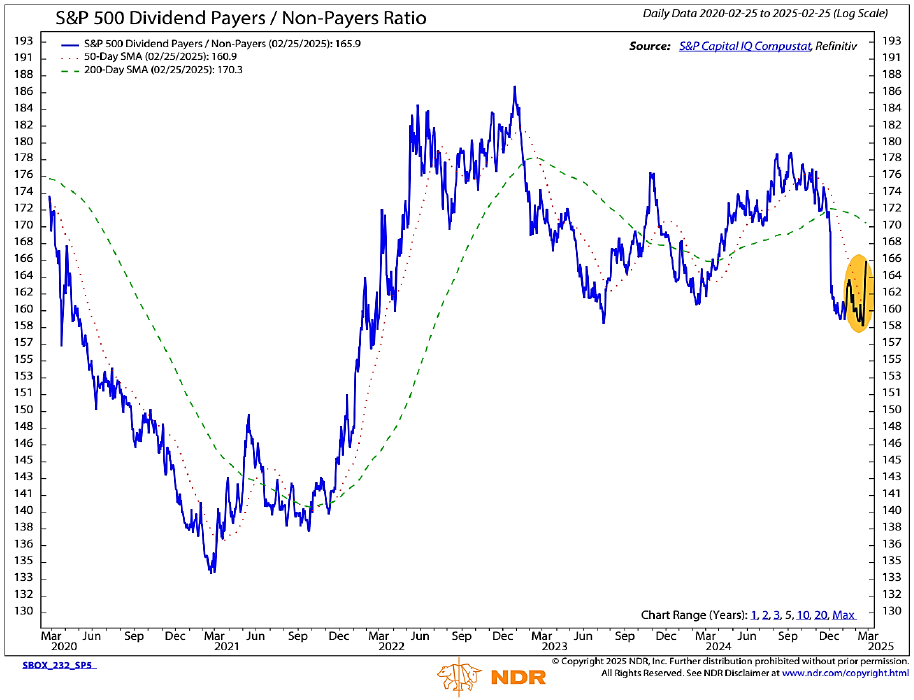

Conversely, dividend payers have perked up after underperforming materially since the 50 bp rate cut. What gives? We believe that with the Federal Reserve (Fed) signaling mid-month that interest rates may remain closer to their 2023 high than they expected due to persistent inflation concerns, the prospects for a more challenging macroeconomic environment increased the appeal for dividend-paying stocks. Our observation is that the aggressive monetary policy in late 2024 accentuated momentum linked to earnings revisions, especially in economically sensitive stocks with non-payers outperforming dividend payers, as seen in the chart above. With the Fed signaling less stimulus in 2025, we may see more of a balance in stock performance between dividend payers and non-payers.

As always, thank you for your interest and trust managing your investments.

About the Author

Charles Wittmann, CFA®, Executive Director, joined SCM in 2014 and has investment experience since 1995. Chip is Co-Portfolio Manager of the Equity Income strategy. Prior to joining SCM, he worked for Thompson Siegel & Walmsley as a portfolio manager and (generalist) analyst. Prior to TS&W, he was a founding portfolio manager and analyst with Shockoe Capital, an equity long/short hedge fund. Chip received his B.A. in Economics from Davidson College and his M.B.A. from Duke University's Fuqua School of Business. He holds the Chartered Financial Analyst® designation and served as President of CFA Society Virginia from 2012-2013.

Related Insights

08.25.2025 • Andrew Richman, CTFA

08.05.2025 • Charles Wittmann, CFA®

07.02.2025 • Charles Wittmann, CFA®

06.20.2025 • Andrew Richman, CTFA

Explore