One of the main reasons for this publication is to share with clients and prospective investors what we do, why, and how we invest. We believe that as portfolio managers, owning material amounts of the strategy that we manage and sharing how we manage the strategy with clients can further align our interests to maximize the potential for successful long-term results.

We have shared the qualities we seek in the companies we invest in and how we research their perceived competitive advantage, but what advantage can an investor have? We have found there are three sources of investor competitive advantages. The first is information - knowing what no one else does. The second is analytical, absorbed public information and coming to a better conclusion. The third is a behavioral advantage by employing a different psychology. We believe to pursue investment success one may have to be different from the crowd, and one observation we would make is that the crowd is not patient. According to the New York Stock Exchange (NYSE) and Refinitiv, the average holding period for shares on the NYSE in 2020 was 5.5 months. For some historical perspective, in the late 1950s it was eight years, in the 1970s it was around five years, and in 1999 it was fourteen months.

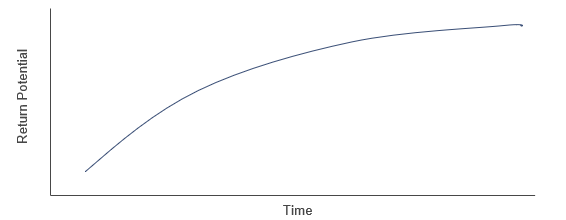

We have used the term “ripple in the matrix” to describe a temporary dislocation in a stock price that can pave the way for generating value along the equity yield curve, a concept developed by Steven Bregman. This concept is shared in the chart above. The dislocation can occur when a stock’s share price meaningfully separates from its long-term business prospects. Such a dislocation can occur during earnings seasons such as the one we are in now, where short-term earnings miss the expectations set by Wall Street analysts.

Emotions of the moment, the quest for short-term results, and perhaps financial media reporting can create confusion in using short-term information to price a security. As investors scramble for the incremental data point, they may find it is a highly competitive exercise as that is where most market participants do their work. Don’t believe us? In 2022, we noted that a Bloomberg transcript search of S&P 500 companies halfway through the first quarter of that year had the words “next quarter” mentioned 596 times and the words “next decade” spoken only 30 times.

1986 - 2013

What’s going on when two investors are accessing the same quarterly results but making different assessments? We believe we respond to a completely different set of stimuli than other participants by employing different cognitive functions. In our opinion, the benefit to focusing on the long end of the equity yield curve is there are fewer competitors.

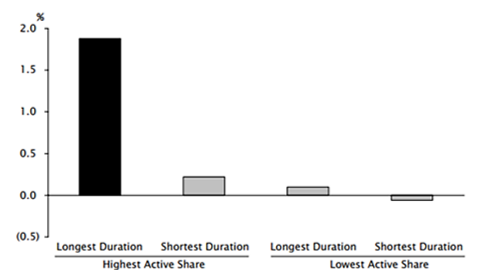

The concept of the equity yield curve is helpful to visualize how patience can create value. Rather than incur transaction costs by trading and competing at the short end of the curve, by seeking out advantaged companies and enabling them to earn their path to value, we believe we position clients for success. The Empirical Research study above supports the benefits of a differentiated long-term approach (long duration) to generate outperformance. By building high active share portfolios (different than the market) and utilizing a longer-term approach, we seek to combine the best of these demonstrated approaches to investing.

As always, thank you for your interest and trust managing your investments.

About the Author

Charles Wittmann, CFA®, Executive Director, joined SCM in 2014 and has investment experience since 1995. Chip is Co-Portfolio Manager of the Equity Income strategy. Prior to joining SCM, he worked for Thompson Siegel & Walmsley as a portfolio manager and (generalist) analyst. Prior to TS&W, he was a founding portfolio manager and analyst with Shockoe Capital, an equity long/short hedge fund. Chip received his B.A. in Economics from Davidson College and his M.B.A. from Duke University's Fuqua School of Business. He holds the Chartered Financial Analyst® designation and served as President of CFA Society Virginia from 2012-2013.

Related Insights

10.07.2025 • Charles Wittmann, CFA®

10.03.2025 • Michael McVicker

09.24.2025 • Tom O'Toole

09.09.2025 • Charles Wittmann, CFA®

Explore