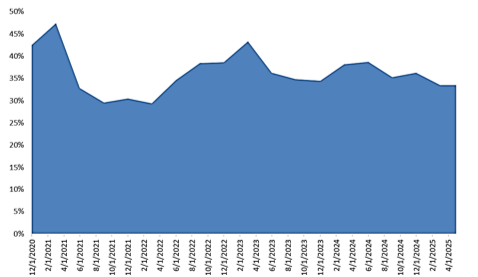

Throughout this year we have touched on the many unique aspects of 2025, including how certain characteristics may have impacted equity market returns and could have caused certain styles to perform. As we enter the month of December, we thought it would be helpful to take stock in what we believe has worked thus far in 2025 for market participants. Arguably, what we see as the most unique aspect of this year is how we seem to be in the midst of the biggest run for momentum stocks in the past seventy years. Momentum investing is when investors buy securities that are already rising-stocks that are “up” keep going “up.” The combination of retail investors with trend-following strategies have possibly helped fuel this trend, especially since April of this year. The chart to the right depicts the relative performance of momentum stocks recently and places the relative performance in historical context.

Within momentum stocks this year, what has been working? As seen in the chart above, it has been lower quality stocks based on S&P quality rating methodology. The chart groups overall quality in the yellow bars, but as can be seen, year-to-date within the low-quality cohort, it has been the lowest quality stocks that seem to have performed the best. Moreover, the difference has been striking, with the lowest quality stocks outperforming the next category by over 10%, and overall low-quality outperforming by over 8% through October.

About the Author

Charles Wittmann, CFA®, Executive Director, joined SCM in 2014 and has investment experience since 1995. Chip is Co-Portfolio Manager of the Equity Income strategy. Prior to joining SCM, he worked for Thompson Siegel & Walmsley as a portfolio manager and (generalist) analyst. Prior to TS&W, he was a founding portfolio manager and analyst with Shockoe Capital, an equity long/short hedge fund. Chip received his B.A. in Economics from Davidson College and his M.B.A. from Duke University's Fuqua School of Business. He holds the Chartered Financial Analyst® designation and served as President of CFA Society Virginia from 2012-2013.

Related Insights

03.11.2026 • Charles Wittmann, CFA®

02.11.2026 • Charles Wittmann, CFA®

01.13.2026 • Charles Wittmann, CFA®

12.09.2025

Gregory Zage, CFA®, Justin Nicholson

The Sterling Capital VAULT: Passive Investing is NOT Static Investing