(Price Performance as of December 31, 2025)

Our purpose with this publication over the years has been to describe how changing markets may impact investment philosophies and style so that investors could be well informed. During certain periods, market anomalies may be historic in terms of their magnitude and impact on stock price performance, albeit temporary. In prior months we have touched on the magnitude that both risk (beta) and momentum may have exhibited in 2025. We believe the flip side of the coin for these characteristics is typically quality.

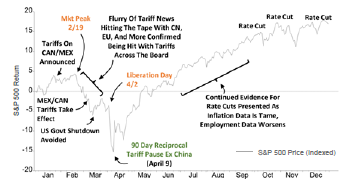

In strong market conditions, such as the post Liberation Day market, falling tariff fears, and the potential for federal funds rate cuts led to a boost in upward earnings expectations to levels not seen since the end of the global financial crisis and Covid-19 (captured in the graphic below).

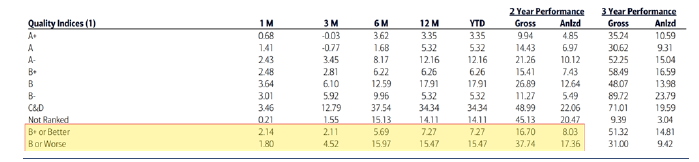

The result is shown in the highlighted portion of the graphic that shows the difference in performance between higher quality and lower quality stocks in the market. In fact, quality was the worst performing characteristic of the ones BofA Global tracked in 2025. The chart below uses S&P’s formula for assigning a quality letter grade to stocks based with higher grades for return on capital, stronger balance sheets, and earnings stability. To place the performance challenges of quality in perspective, we gathered data from BofA Global that combined equally weighted performance of quality and earnings stability trends over the past 20 years.

Moreover, stocks with the highest valuations in the market also appear to have been the best performers. In the chart on this page we show how the most expensive stocks on an earnings basis (Quintile 1 stocks) have been the best performers with the least expensive stocks lagging year-to-date. We believe the bull case, or optimism for a continuation of this trend is that the possibility of additional Federal Reserve rate cuts this month and next year may help propel overall earnings growth to double digit levels in 2026.

Given the dynamics in 2025, we have been finding value in companies with high returns on equity, stable earnings growth, and low debt levels. In our opinion, the environment in 2025 has seemed to provide unique investment opportunities in companies that possess these traits.

As always thank you for your interest and trust managing your investments.

The difference in material performance last year highlighted two contrasting investment characteristics, risk and quality. Risk can be driven by market forces such as unusually strong spikes in earnings revisions which may be fueled by fiscal or monetary stimulus creating an appetite for risk taking, as in stocks for example. We would contrast these bursts with the longer term performance of high returns on capital and earnings growth stability.

It is during short periods of V-shaped bursts of upward earnings expectations that quality styles can experience challenges, although in our view they tend to be temporary as the sugar rush eventually fades.

As always thank you for your interest and trust managing your investments.

About the Author

Charles Wittmann, CFA®, Executive Director, joined SCM in 2014 and has investment experience since 1995. Chip is Co-Portfolio Manager of the Equity Income strategy. Prior to joining SCM, he worked for Thompson Siegel & Walmsley as a portfolio manager and (generalist) analyst. Prior to TS&W, he was a founding portfolio manager and analyst with Shockoe Capital, an equity long/short hedge fund. Chip received his B.A. in Economics from Davidson College and his M.B.A. from Duke University's Fuqua School of Business. He holds the Chartered Financial Analyst® designation and served as President of CFA Society Virginia from 2012-2013.

Related Insights

03.11.2026 • Charles Wittmann, CFA®

02.11.2026 • Charles Wittmann, CFA®

12.11.2025 • Charles Wittmann, CFA®

12.09.2025

Gregory Zage, CFA®, Justin Nicholson

The Sterling Capital VAULT: Passive Investing is NOT Static Investing