One might wonder if we are using the appropriate benchmark for the Equity Income strategy since we own a large capitalization software company that is commonly classified in databases as a large cap growth stock. We think this is an appropriate question as professionals in manager research are tasked with assessing if a manager is "true to style.” If they are allocating assets to a value manager, will their performance correlate to the value benchmark? If investment manager returns are different from the benchmark, is it due to skill or that their holdings are not representative of the benchmark against which they are being measured?

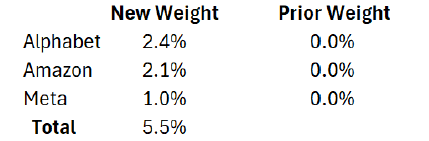

Why would several mega-cap stocks that have been classified as 100% growth in the past be classified, even partially, in value? FTSE Russell uses an objective style and methodology that splits the Russell 1000® Index into growth or value based primarily on earnings growth, sales growth, and price-to-book measures (the last reconstitution was June 27, 2025). One constraint is that Russell 1000® Growth and Russell 1000® Value Indexes need to total the core Russell 1000. An example of this challenge is Amazon, which was 3.6% of the Russell 1000 at the time of reconstitution. Instead of assigning a full 3.6% change to the value benchmark, Russell has announced its partial weight is now 2.1% based on its criteria, as seen in the table to the right.

In the table, Russell points to each of these stocks’ improved price-to-book valuations and modestly slower growth characteristics for the reclassification, in addition to the maturation of their businesses given their size. We believe that other dynamics play a role. We feel that the sizeable weights of these mega-cap stocks in the overall index, while keeping the growth and value indexes the same size, achieve the stated desire to minimize turnover. Through partial weights, there may be fewer annual switches of stocks between the growth and value indexes in an effort to minimize the changes investors who want to mimic the benchmarks may need to make when tracking them.

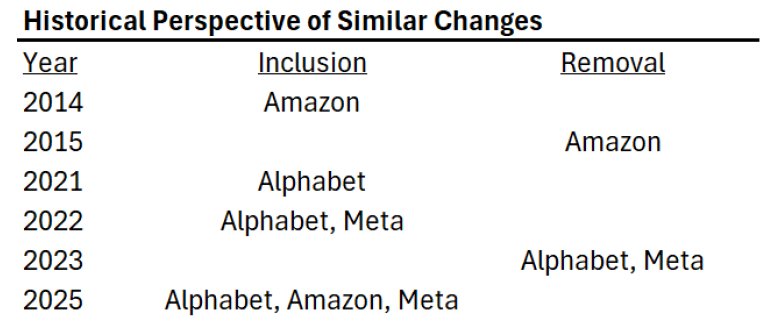

The table at the top of the page showcases a situation that we have seen happen before, notably in 2022 when several notable growth stocks were classified as value for a year. Only twelve months later, those stocks were gone from the index. It was a short-lived visit

“as a value stock” from our perspective.

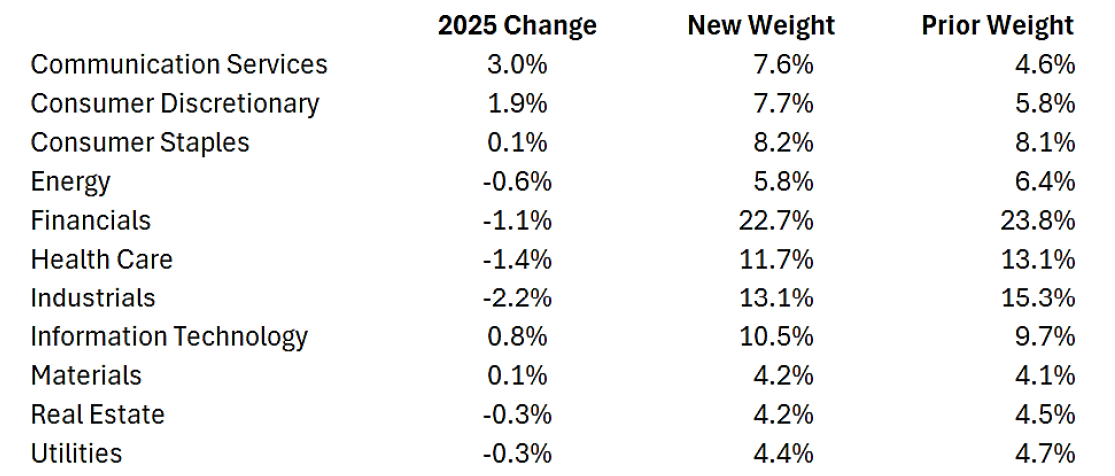

In the meantime, we believe the inclusion of these names may have an impact on the overall complexion of the economic sector weights of the index, notably Communication Services, as seen in the chart above. What is interesting to us is that many times, it is the benchmark making short-term oriented changes, not the manager’s investment philosophy or style. We have held a large cap software stock for over a decade that has been classified differently during our holding period. We kept it because we believe it is consistent with our investment philosophy and mandate over the past decade, while acknowledging there have also been short-term annual entrances and exits by certain stocks in our benchmark. When asked if we plan to change our investments for the changes in the benchmark, the answer is we are aware of the changes, and our focus remains committed to the same process and mandate that has stood for decades.

As always, thank you for your interest and trust managing your investments.

About the Author

Charles Wittmann, CFA®, Executive Director, joined SCM in 2014 and has investment experience since 1995. Chip is Co-Portfolio Manager of the Equity Income strategy. Prior to joining SCM, he worked for Thompson Siegel & Walmsley as a portfolio manager and (generalist) analyst. Prior to TS&W, he was a founding portfolio manager and analyst with Shockoe Capital, an equity long/short hedge fund. Chip received his B.A. in Economics from Davidson College and his M.B.A. from Duke University's Fuqua School of Business. He holds the Chartered Financial Analyst® designation and served as President of CFA Society Virginia from 2012-2013.

Related Insights

11.11.2025 • Charles Wittmann, CFA®

10.30.2025 • Andrew Richman, CTFA

Fed Cuts Rates Again, But Additional Cuts Are Not Guaranteed

10.23.2025 • Charles Wittmann, CFA®

10.03.2025 • Michael McVicker

Explore