The term “summer doldrums” originated from a nautical term describing a belt of low pressure around the equator, creating windless conditions where sailing ships were becalmed for days. This summer, the stock market has exhibited anything but “summer doldrums.” The stock market rebound off the “Liberation Day” lows has been robust, in our view, with certain areas of the market rebounding more aggressively than others.

The core purpose of our monthly piece is to share the underlying drivers and trends in the stock market. We want clients to fully understand the characteristics driving the market and the contributors to performance so they can better understand their investments. This summer, we found it difficult to find an area that has experienced greater historic performance than high beta stocks (stocks with higher calculated volatility or price swings relative to the market as a whole). They are generally considered as stocks with greater risk given their price swings. In the chart at the top of the page, we can see that high beta stocks relative to low beta stocks are experiencing a rare divergence in performance. Over the last 25 years, we have only seen this level of divergence in 1% of the observations.

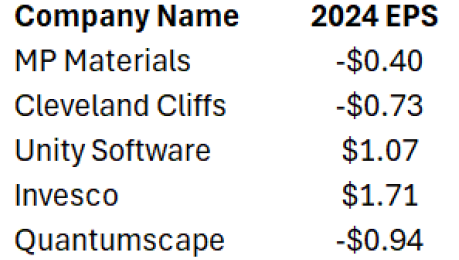

To provide some perspective on why high beta stocks may be considered riskier while linking the risk to fundamentals, we provided a table below with the top five performers in our benchmark this month. The average of this cohort of stocks meets the definition of high beta, and as one can see, the majority have been unprofitable over the past year.

Over the past year, we have seen investors embrace and shed risk in dynamic fashion. The chart above shows that over the past year, high beta performed well in late 2024, largely underperformed in March and April of this year, then rebounded aggressively since April. The chart is also supported by credit spreads, which is another measure of risk. Given where high beta stocks reside today, a return to more balanced performance could bode well for less risky, profitable stocks.

As always, thank you for your interest and trust managing your investments.

About the Author

Charles Wittmann, CFA®, Executive Director, joined SCM in 2014 and has investment experience since 1995. Chip is Co-Portfolio Manager of the Equity Income strategy. Prior to joining SCM, he worked for Thompson Siegel & Walmsley as a portfolio manager and (generalist) analyst. Prior to TS&W, he was a founding portfolio manager and analyst with Shockoe Capital, an equity long/short hedge fund. Chip received his B.A. in Economics from Davidson College and his M.B.A. from Duke University's Fuqua School of Business. He holds the Chartered Financial Analyst® designation and served as President of CFA Society Virginia from 2012-2013.

Related Insights

02.11.2026 • Charles Wittmann, CFA®

01.13.2026 • Charles Wittmann, CFA®

12.11.2025 • Charles Wittmann, CFA®

12.09.2025

Gregory Zage, CFA®, Justin Nicholson

The Sterling Capital VAULT: Passive Investing is NOT Static Investing