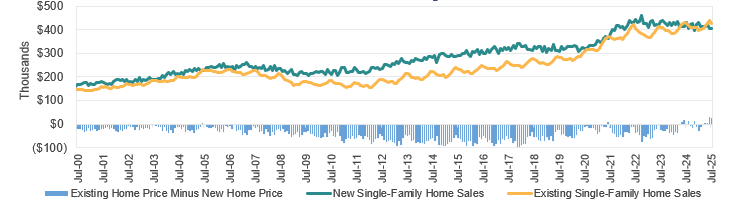

Since 2020, the premium for a new home has declined versus the median home price of an existing home and, aside from a pandemic-induced blip in 2021 when the cost of capital was historically cheap, the median price for an existing home is now sustainably above that of a new home. Historically, new homes are priced at a premium to existing homes due to newer materials, construction standards, and updated features and designs. What’s happening?

Lock-In Effect

Mortgage rates and home prices (both new and existing) soared post-pandemic and changed the calculus on the cost of homeownership. Since 2022, more homeowners hold a below-market rate on their existing mortgage and would face higher borrowing costs on a new mortgage. Homeowners are no longer opportunistically moving as they were in 2021. The Federal Housing Finance Agency estimates that every 1% increase in the gap between a borrower’s existing rate and the market rate cuts sales probability by 18%. As of Q1 2025, 71.3% of outstanding mortgages are below 5%, with the average at 4.3%.

Supply

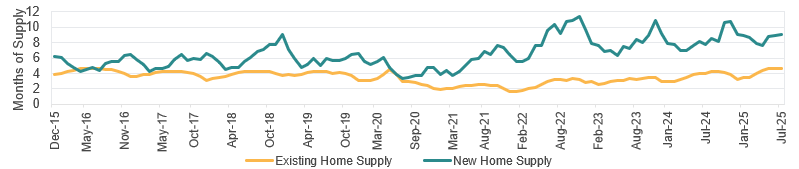

As potential homebuyers opt to remain in their existing homes with their below-market rate, the supply of existing homes has fallen below historical averages. Meanwhile, homebuilders have attempted to fill that gap by accelerating production of new homes. This dynamic is pressuring new home prices lower and existing home prices higher.

Smaller Homes

Builders have reduced the size of the homes they build. The median square footage of a new single-family home declined to approximately 2,140 square feet as of Q1 2024, the smallest since 2009. If a prospective buyer wants a larger home, they’ll likely need to turn to the undersupplied existing home market. However, as discussed, many existing homeowners are locked into their below-market rate mortgages and are not incentivized to move.

About the Author

Tom O’Toole, Director, joined SCM in 2022 and has investment experience since 2018. He is a Senior Fixed Income Credit Analyst. Prior to joining SCM, he was a senior manager at the Korea Investment Corporation sovereign wealth fund in New York where he was responsible for portfolio management, idea generation and credit analysis for Investment Grade and also had some trading responsibilities. Tom graduated from UNC Wilmington with a BSc in Business Administration with a specialty in Finance and has an MBA from Notre Dame.

Related Insights

11.11.2025 • Charles Wittmann, CFA®

10.30.2025 • Andrew Richman, CTFA

Fed Cuts Rates Again, But Additional Cuts Are Not Guaranteed

10.23.2025 • Charles Wittmann, CFA®

10.03.2025 • Michael McVicker

Explore