Artificial intelligence (AI) and the related datacenter buildout have been the predominant themes in capital markets over the past several years, driving capital expenditures and powering certain large-cap equities into mega-cap status. However, gaining exposure to AI datacenters in the fixed income market is not as straightforward as simply owning the “Magnificent Seven” stocks. The fixed income market offers investors over $300B worth of options, ranging from corporate debt to club deals to various flavors of securitized products. How investors choose to gain datacenter exposure can be as custom as toppings on an ice cream sundae. Let’s dig in.

Investment-Grade Hyperscaler Corporate Debt:

- Frequent, multi-tranche corporate bond deals from Amazon, Google, Meta, Microsoft, and Oracle.

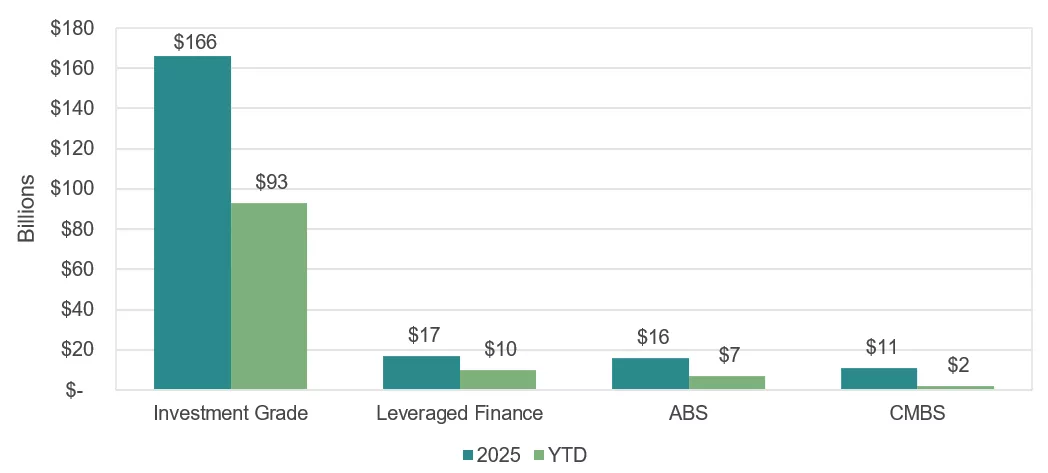

- Historically, hyperscalers have not been active issuers. However, hyperscaler issuance increased from $17B in 2024 to $121B in 2025. $82B has already been issued in 2026.

- Despite the rapid increase in debt issuance, credit quality has remained. Four of the five hyperscalers are rated AA or higher.

- Issuance has been across the curve in multiple currencies. Google was able to issue a 100-year bond in GBP.

- Some issuers are also creatively issuing debt though special purpose vehicles (SPVs) that are off-balance sheet, such as last year’s Beignet deal and, most recently, the Quality Technology Services (QTS) deal. These deals tend to offer additional spread relative to what their ratings would otherwise suggest.

High Yield and Leveraged Loans:

- Issuers are also using the SPV model to issue in the high yield market.

- These are differentiated structures where the debt is issued out of a SPV and the hyperscaler provides various forms of credit enhancement and structural protection such as parent guarantees, funded reserve accounts, and amortizations.

- These deals are effectively a form of project finance. First-lien AI infrastructure bonds are backed by long-term hyperscaler cash flows rather than traditional unsecured high yield bonds issued against a volatile operating business.

Asset-Backed Securities (ABS):

- These securities are backed by the operating cash flows of the datacenter, primarily tenant lease receivables.

- Collateral typically includes leases, physical infrastructure, and operating contracts, with a focus on the durability of the operating platform rather than pure property value.

- Datacenter ABS tenant types are primarily segmented into hyperscalers and colocation. Hyperscalers include larger, more highly-rated technology companies, while colocation deals have multiple tenants of mixed credit profiles which may be more commercially oriented.

- Funding datacenters in the ABS market began in earnest in 2020. As of YE 2025, datacenter ABS outstanding was $36.6B, which represented 4.6% of all ABS outstanding. The datacenter market share has doubled from 2.3% in 2023 as the sector has rapidly expanded.

- ABS datacenter issuance totaled $16B in 2025 and is expected to increase to $25-30B in 2026, according to Deutsche Bank.

Commercial Mortgage-Backed Securities (CMBS):

- Secured by a mortgage on a specific property or campus, usually structured as a single-asset, single-borrower (SASB) loan.

- The underlying data centers are typically stabilized, fully-leased assets located in major demand hubs with strong power availability and supporting infrastructure.

- Key considerations include:

- Newer facilities that may be well positioned to benefit from growing AI-driven demand with limited risks of technological obsolescence.

- Assets with long-term leases in place with high-quality, credit tenants, where lease terms extend close to or beyond loan maturity and tenants are likely to renew.

- SASB CMBS datacenter issuance totaled $11B in 2025 and is expected to exceed $15B in 2026, according to Deutsche Bank.

Related Insights

07.14.2026 • Charles Wittmann, CFA®

06.23.2026

Gregory Zage, CFA®, James Kerin, CFA®

05.11.2026 • Charles Wittmann, CFA®

04.13.2026 • Charles Wittmann, CFA®