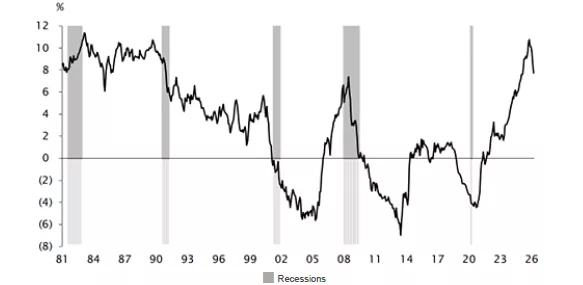

The Relative Returns of the Top Quintile of Earnings Revisions Monthly Data Compounded to Annual Periods — Trailing Five-Year Averages 1981 to Mid-March 2026

As we are in the midst of college basketball teams striving to win and move onto the next round of the NCAA tournament, we’d like to take a look at what has been winning in the market since March of last year. As we shared a year ago, we believe that momentum has been a driving force not only through March of last year, but through the past twelve months. We’ve noted that momentum can consist of price momentum, where stocks that are rising in price may continue to do so into the future. Many times price momentum is coupled with earnings momentum, where stocks that report earnings surprises above Wall Street analysts’ expectations could continue to do so quarter after quarter.

This month Empirical Research Partners provided additional data around this notable period for the performance of earnings revisions, coupled with their observation that recent price momentum has been the strongest in seven decades. There are two important observations from this information that may impact clients’ understanding of their investments.

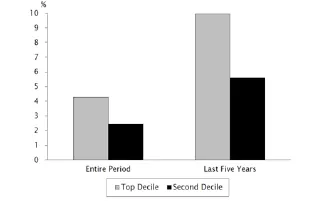

First, their data shows that the 2020’s have seen the strongest performance for earnings revisions since the 1980’s. As the chart at the top of the page shows, since 2020, the top 20% of large capitalization stocks with upward revisions have driven relative performance. The second chart on this page puts the performance over the last five years in perspective, going back even further to 1976.

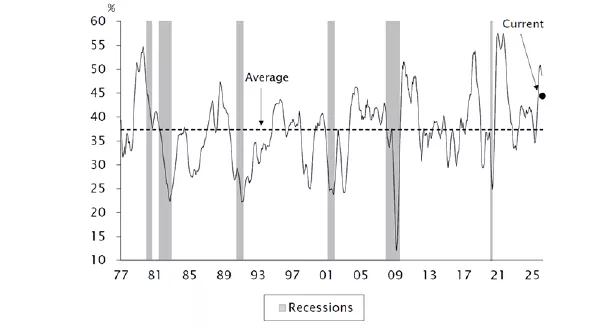

The Relative Returns of the Top Two Deciles of Earnings Revisions — Monthly Data Compounded to Annual Periods 1976 to Mid-March 2026

The chart above shows that the percentage of stocks experiencing upward earnings revisions has been more positive than in the past, both during the recovery from the Pandemic and from the recent artificial intelligence capital investment spike in 2025. Our observation is that the strong performance of earnings revisions has been reflected in higher valuations for these securities that historically exhibited more stable and consistent earnings patterns.

As always thank you for your interest and trust managing your investments.

About the Author

Charles Wittmann, CFA®, Executive Director, joined SCM in 2014 and has investment experience since 1995. Chip is Co-Portfolio Manager of the Equity Income strategy. Prior to joining SCM, he worked for Thompson Siegel & Walmsley as a portfolio manager and (generalist) analyst. Prior to TS&W, he was a founding portfolio manager and analyst with Shockoe Capital, an equity long/short hedge fund. Chip received his B.A. in Economics from Davidson College and his M.B.A. from Duke University's Fuqua School of Business. He holds the Chartered Financial Analyst® designation and served as President of CFA Society Virginia from 2012-2013.

Related Insights

07.14.2026 • Charles Wittmann, CFA®

06.23.2026

Gregory Zage, CFA®, James Kerin, CFA®

05.11.2026 • Charles Wittmann, CFA®