During our research meeting last week, the investment team was scrutinizing three of our equity investments. A topic that kept surfacing while determining which stock we believed had the best prospect for outperformance was capital allocation. How a company manages the capital we provide to them as equity investors provides us with insight into their business acumen, their priorities, and their ability to plan growth for their business. We believe one of the beauties of dividend growth investing is that companies with a history of sharing their earnings through dividend payments to their shareholders, and increasing those dividends, provides us with valuable insight into their priorities and their ability to pay amounts that may grow over time.

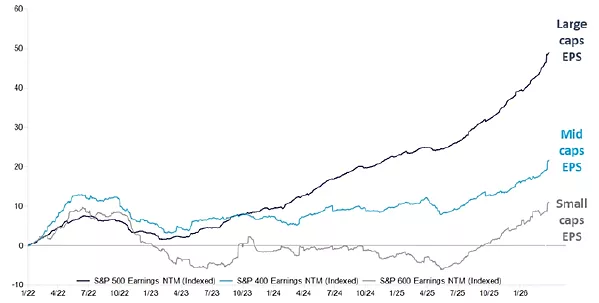

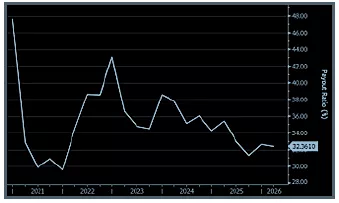

A function of this dynamic is the dividend payout ratio that measures the percentage of earnings that companies return to shareholders through dividend payments each period. As can be seen in the chart at the top of the page, the trend for earnings for companies large and small has been up and to the right. Have these growing earnings streams been shared with shareholders? Maybe not to their potential, in our view.

There are a number of possible value enhancing areas where company management may apply a portion of earnings, such as share repurchases, for example. But despite higher corporate earnings, the percentage shared with their shareholders appears to have been falling over the past several years.

As a result of these lower dividend payout ratios, we believe this may be a situation where higher levels of corporate earnings are not translating into dividend growth in the market or the S&P 500, as seen in the chart above. We seek out quality companies that may not only grow earnings but generate returns on capital in excess of the demands to grow the business, so they may also deliver dividend growth commensurate with their earnings growth. If there is value in scarcity with dividend growth, companies that not only pay dividends but grow them faster than the market appear to have a valuable quality. We prefer companies that share wealth year in and year out.

As always thank you for your interest and trust managing your investments.

About the Author

Charles Wittmann, CFA®, Executive Director, joined SCM in 2014 and has investment experience since 1995. Chip is Co-Portfolio Manager of the Equity Income strategy. Prior to joining SCM, he worked for Thompson Siegel & Walmsley as a portfolio manager and (generalist) analyst. Prior to TS&W, he was a founding portfolio manager and analyst with Shockoe Capital, an equity long/short hedge fund. Chip received his B.A. in Economics from Davidson College and his M.B.A. from Duke University's Fuqua School of Business. He holds the Chartered Financial Analyst® designation and served as President of CFA Society Virginia from 2012-2013.

Related Insights

07.14.2026 • Charles Wittmann, CFA®

06.23.2026

Gregory Zage, CFA®, James Kerin, CFA®

04.13.2026 • Charles Wittmann, CFA®