Coming off what we believe to be an historic quarter for momentum, it is helpful to keep in mind two very important benefits of investing in equities. One is the power of compounding value over time, and second is the benefit of diversification to generate attractive risk adjusted returns.

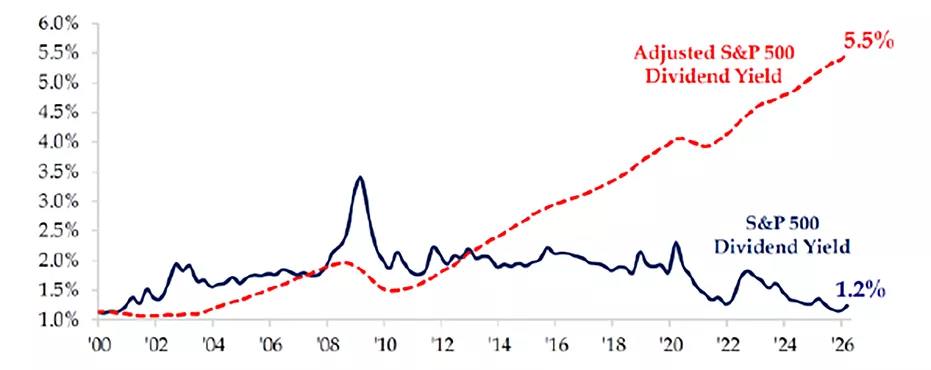

In the current market, traditional characteristics of classic long-term investing, such as sustainable earnings growth and its potential byproduct of paying increasingly higher dividends over time, seem to us to have been pushed to the side. While dividend yield appears to be in short supply in the current market, the potential benefits of compounding dividends over time remain significant as seen in the graphic at the top of the page.

Similar to other periods in market history, sectors of the market that have historically demonstrated high returns on capital, strong balance sheets and earnings stability, possibly due to their advantaged competitive positions, have seen their relative market capitalizations shrink. This group now represents the smallest share of the market in its history.

We see this dynamic as potential opportunity. The chart on the next page shows the relative valuation for low volatility stocks that tend to have the characteristics we just outlined. Historically, as the line in blue shows, these stocks typically trade at a premium because of their attractive fundamental characteristics. But it appears not in this market, as they are trading at a historic discount.

While strong fundamentals and market positions coupled with the prospects for growing earnings through more efficient operations sound attractive, in our opinion, the reason for our pursuit of these opportunities lies in their historical track record for generating outperformance over time. The second chart on the first page shows the performance of earnings stability, its performance over the past year and its long- term performance pattern. Our constructive outlook is tempered with an awareness of elevated inflation and low unemployment, which may challenge the prospect of lower rates and leave the door open for a higher federal funds rate, especially with continued strong gross domestic product (GDP) growth.

We also remain mindful of overall valuations that imply elevated expectations and the current market concentration within major market indices.

As always thank you for your interest and trust managing your investments.

About the Author

Charles Wittmann, CFA®, Executive Director, joined SCM in 2014 and has investment experience since 1995. Chip is Co-Portfolio Manager of the Equity Income strategy. Prior to joining SCM, he worked for Thompson Siegel & Walmsley as a portfolio manager and (generalist) analyst. Prior to TS&W, he was a founding portfolio manager and analyst with Shockoe Capital, an equity long/short hedge fund. Chip received his B.A. in Economics from Davidson College and his M.B.A. from Duke University's Fuqua School of Business. He holds the Chartered Financial Analyst® designation and served as President of CFA Society Virginia from 2012-2013.

Related Insights

06.23.2026

Gregory Zage, CFA®, James Kerin, CFA®

05.11.2026 • Charles Wittmann, CFA®

04.13.2026 • Charles Wittmann, CFA®